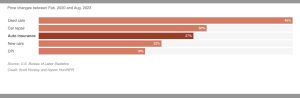

The cost of new vehicles – which now “transact” for about $50k on average – is such that a large and growing number of people can no longer afford them. That’s not so bad, though – right? Because no one has to buy a new vehicle. True. But the cost of insuring the vehicle you have has been going up double digits annually – 25 percent, on average – for the past two years.

If this continues, what then?

Many people who were paying very little for a liability-only policy – which everyone who owns a car is required by law to buy as the condition of being allowed to drive – are now paying a lot more, even though they have not done anything to justify the double-digit increase in the cost of this coverage, which doesn’t actually cover anything except the hypothetical cost of repairing damage to some other person’s vehicle, if the “insured” is involved in an accident with some other person’s vehicle.

If that vehicle is someone else’s late-model $50,000 (or more) vehicle, it will cost hugely to repair it or – if the damage is bad enough – replace it. That anticipated cost is transferred onto the shoulders of the people who did not buy the $50,000 (or more) vehicle – or damage it. It is merely the hypothetical that justifies the actual – in the form of the double digit increase in the cost of this coverage.

Now, play this out a little.

Is the cost of new vehicles continuing to go up? What will happen to the cost of insurance when a new vehicle transacts for $60,000? We’ll all be paying for that.

Some won’t be able to – and then they won’t be allowed o drive (legally).

A person who does not own a $50,000 (or more) vehicle who was paying $300 annually for a basic, liability-only policy on his low-book-value old vehicle – which he keeps because he does not want to (or cannot afford to) take on the $800 monthly payment it takes to finance a $50,000-ish vehicle over six years – is being gradually pushed into making insurance payments that he eventually will not longer be able afford to make. Because other people choose to buy $50,000-plus vehicles – and because he is forced to pay what it costs to “cover” repairs to these vehicles.

Axiom:

Whenever you’re forced to buy something, that something is going to cost more rather than less. The cost of insurance coverage is no different.

Consider what happened to the cost of a simple, “catastrophic care” only health insurance policy that pays for nothing routine and only for the costs of extreme events unlikely to happen, such as a stroke. The cost of this coverage was reasonable – until the federal government (under Obama) decreed that everyone and everything be “covered,” including routine check-ups and tests. Naturally, these tests and so on became very expensive and everyone who was forced to buy insurance got to pay for that, even if they themselves avoided going to the doctor unless they really needed to.

Presto! Health insurance – a silly term, when you think about it a little since no one’s health can be insured – now costs so much working and middle income people can’t afford it. But they are forced to pay for it.

Car insurance at government-point works the same way. When you’re not allowed to say no – and when you’re forced to assume the burden of hypothetical costs imposed by other people, whose decisions you have no control over whatsoever, is it surprising that the cost of insurance has increased by double digits over just the past couple of years? The question now is: How much more will it increase – and how long will it be before people in large numbers are priced out of owning a vehicle, even a low-value old one, on account of being unable to pay for the insurance the government requires they carry?

It will likely not be long – given the rising cost of everything else.

Groceries, for instance. A $100 bill that used to buy a shopping cart full of staples now bags two plastic bags of them. In most parts of the country, the cost of the property taxes homeowners (sic) are forced to pay in order to avoid being evicted from what is of course not actually their home has also gone up – especially in the rural (and red) areas where these taxes were once low, on account of hordes of refugees from red areas moving into those areas to escape the high cost of living in a red area and bringing those costs with them. They often build huge homes twice the size of the modest homes in the area and thus – via raised assessments – increase the cost of the natives’ taxes, very much in the way that the affluent few who can afford to buy a $50,000 (and more) vehicle pass on the costs to those who didn’t buy one.

It is pretty obvious that owning and driving a car is becoming a kind of luxury – and luxuries are things most people cannot afford. It is not difficult to see where this leads. Whether intentional or not, the end result is the same. Working and middle income people (such as are left) will inevitably be forced to give up owning and driving cars they can no longer afford to insure.

We’ll know whether it is by design if nothing is done to ease the burden on those who are not incurring the costs.

This could be done in a free market-ish manner by limiting the cost of mandatory insurance coverage to covering the cost of repairing or replacing hypothetical losses up to say $30,000 – which would cover modestly priced vehicles. Let those who choose to buy a vehicle that costs more than $30,000 buy additional coverage to offset the cost of potential losses.

It’s entirely reasonable and so entirely fair.

And that’s exactly why it’s as likely to happen as Fauci being manacled and sent to prison for the rest of his miserable life.

. . .

If you like what you’ve found here please consider supporting EPautos.

We depend on you to keep the wheels turning!

Our donate button is here.

If you prefer not to use PayPal, our mailing address is:

EPautos

721 Hummingbird Lane SE

Copper Hill, VA 24079

PS: Get an EPautos magnet or sticker or coaster in return for a $20 or more one-time donation or a $10 or more monthly recurring donation. (Please be sure to tell us you want a magnet or sticker or coaster – and also, provide an address, so we know where to mail the thing!)

If you’d like a Baaaaa hat or other EPautos gear, see here!

{kind=link}

Happened to notice on my insurance that my 3/4 ton Chevy and 1 ton winch truck were listed as for “pleasure and school”. I don’t go to school anymore and I don’t typically drive a winch truck for “pleasure”. Had them changed to farm use and saved about $100.

Some states, most notably Florida and Texas, exempt primary residences from seizure. That is why OJ Simpson was able to keep his house in Florida after being sued.

[…] More […]

When did any level of government in this alleged constitutional republic acquire the ability to mandate any free man to do or buy ANYTHING?

Insurance is a good idea, if you have something to lose. For most people, it is a terrible bet.

The only result of mandatory insurance is a ready trough of money for the ambulance chasing shyster to feed at. No honest person gains from it.

Eric – can we get your thoughts on the la riots? Paid provacateurs? Useful idiots? Who are these people? Are they good? Bad? Illegals protesting? Vandalizing, setting things ablaze, assaulting, rioting, inciting the mob? Is this normal behavior? I have watched it for 3 days now – all I can say is WAKE UP! Most are being fooled. This is designed to elicit a reaction.

Hi Uknown,

Yes. I think it deserves more than just a quick paragraph; let me make another pot of coffee and have at it. I’ll have something up soon!

Thank you Eric! Look forward to it!

Eric – it is way worse than you think, interest rates are about to skyrocket, rising rates are going to kill auto sales (especially)

see this recent Stew Peters video about what Jamie Dimon said:

https://old.bitchute.com/video/brN0XVD6Wqgn/

Long bond rates are stair stepping higher and a breakout to new highs is imminent. The huge debts can not be paid, government spending is not being curtailed, Trump wants to remove the debt ceiling, etc.

“we are going to see a crack in the bond market, you are going to panic” – quote Jamie Dimon CEO JPMorgan last week

https://bigcharts.marketwatch.com/advchart/frames/frames.asp?show=&insttype=Bond&symb=BX%3ATMUBMUSD30Y&x=42&y=13&time=13&startdate=1%2F4%2F1999&enddate=4%2F10%2F2024&freq=1&compidx=aaaaa%3A0&comptemptext=&comp=none&ma=0&maval=9&uf=0&lf=1&lf2=0&lf3=0&type=4&style=330&size=3&timeFrameToggle=false&compareToToggle=false&indicatorsToggle=false&chartStyleToggle=false&state=9

Around here there is one group aka 13% that is almost exclusively involved in accidents. There is no way that this is inconsequential to the problem of increasing rates.

Hi doo fus,

Yup. And I – like many, I suspect – tire of being held responsible for what others do.

Eric- What about all those cars you test drive- do you have insurance on them? I suppose a dealer or manufacturer could have some kind of General Liability auto insurance, and what about a car lot that lets you take a test drive? You would be the perfect customer for a general liability policy that covers you on every car you drive or test drive. What do you think?

Hi Bill,

The press cars are insured by the manufacturers – i.e., Ford, Toyota, etc. I have another article coming soon about what you’ve brought up…

I can’t get a good explanation from my insurance company why my recently purchased ’03 Toyota Tacoma is twice the price of my ’99 Toyota Tacoma I’ve had for 15 years. The ONLY difference between the two trucks is the ’03 is extended cab and obviously four years younger. EVERYTHING ELSE ABOUT THE TRUCKS ARE EXACTLY THE SAME!!!!! They just say, uh uh uh , it is 4 yrs younger? Boils my blood. That aside, ya’ gotta love the new assessment of property taxes in Floyd County! More than doubled on my property!!!

Hi Rebekah!

Yup. My truck’s old and nothing has changed over the past three years except the cost of the liability-only policy is now more than twice what it was. And – yup, again – re the assessments doubling. I’m also in Floyd – near the Check School – and everyone I know is upset yet we’re just accepting it, I guess. I tried talking to Levi Cox about it but of course he’s a realtor so you know where his bread is buttered….

Texas is a criminal state when it comes to insurance.

Hi Larry,

I think all states qualify as criminal as regards forcing people to buy insurance – for exactly that reason. It is criminal because of the forcing – and because the people being forced have not harmed anyone. The assertion made that they might – and that this justifies forcing them to hand over money to the insurance mafia – is both egregious as such and a very dangerous precedent, for reasons that ought to be obvious. If the government can say: People who drive cars in public must buy insurance because they might cause harm then logically the government could also say that people who carry firearms in public must also “cover” against harms they might cause. The principle – once accepted – is open ended because almost anything might cause harm.

Freedom requires acceptance of the risk that something unfortunate might happen – and even that it sometimes will. Freedom cannot exist when people are not free to assume risks – and enjoy the rewards as well as be held accountable for any consequences that impose harm on others.

But we live among people who want to be “safe.” And that is why we are no longer free.

Go Waymo!

Make Los Angeles burn again!

Self-driving automobiles in Los Angeles have become weapons!

Insurance rates on self-driving vehicles will skyrocket!

Make Illegals Great Again! MIGA!

You would think that Hispanics were Palestinians in LA.

Was Victoria handing out cookies in all of the beaner neighborhoods in Los Angeles?

Doesn’t matter where you are, Kyiv, Los Angeles, Gaza, at this point what difference does it make?

Kill them all!

What would Melania do?

Make the J6 insurrectionists suffer some more!

Morning, Drump !

A point comes when it is every man for himself, as when a ship founders. Well, the ship is foundering – and paying the insurance mafia and obeying the “rules” will soon become optional. Of course, what comes next will either be real freedom – or its opposite.

None of it is actually mandatory….

For starters read this:

https://archive.org/details/police-stop-handout-230307/page/1/mode/1up

Then http://www.sedm.org

Hi Matthew,

Well yes – and no. This comes up a lot. There are valid arguments that prove the law says this – or doesn’t say that. The problem is the law is what those who have power say it is. You are at the mercy of the cop – or the judge. Ask Peter Schiff, whose legal arguments were never disproved as far as the facts. The facts do not matter in an authoritarian system.

Power does.

Looks like that whole hackneyed headline of “half of Americans don’t have $500 for an emergency!” is total BS.

I’m the only person in my neighborhood who washes their own vehicles, as everyone else appears to have pay subscriptions to one of the 900 new automatic car washes that opened in town the past 2 years.

Does anyone make their coffee anymore? There’s a DD or Starbucks for every mile of roadway in the US.

People complain about how expensive fast food is – and then pay additional fees UberEats/GrubHub to drop it on their doorstep.

Plenty of landscaper trucks around for those rich enough to not have to push their own walk-behind.

Too busy to pick up your dog’s waste? There’s a new pay service for that too.

Wake me up when any of this optional and wasteful activity begins to slow.

To paraphrase Twain, “the reports of the death of the US economy are greatly exaggerated.”

Hi Flip,

Well, on the one hand, there are lots of government “workers” who have plenty of our money. The rest of us, on the other hand…

This pisses me off more than almost anything else. There was no insurance required at all when I started driving. It was available if you wanted it. Then along came the ‘liability insurance’ required, except for motorcycles. It was cheap so nobody cared and nothing ever happened unless you were in an accident anyway. People drove around drinking a can of beer all the time, no problem. Then they created ‘drunk driving’ laws and more insurance bullshit. You could deposit $25k or so in an account with the governments name on it instead of having ‘liability’ insurance, but who the hell wants to do that. You can only drive one vehicle at a time, right? One policy for anything I drive while I’m driving it. I can buy contractors general liability insurance why not drivers general liability insurance?

Out in the country in most counties you can drive an off-road vehicle like a Polaris side-by-side, or tractor or farm vehicle on the paved roads if you have a placard displayed and supposedly a $10 off-road vehicle sticker on 4 wheelers. and possibly a driver’s license. Haven’t seen anything said about insurance and there are large areas where people only drive side-by-sides to work and to town and there are hundreds of miles of trails going literally everywhere. Fredericktown, Missouri is one such place.

Morning, Bill!

It pisses me off also. I hugely resent being punished for harms I have not caused – and it is punishment to be forced to hand over money to the insurance mafia for “coverage” and you will be punished in other ways if you fail to buy the “coverage” and get “caught” driving without it – never mind that you haven’t harmed anyone.

Location, location, location.

I moved to the cold. Not many devices here.

My insurance is the cheapest it has ever been. My last renewal, the price went down a few bucks, not up.

Where I’m my insurance went up slightly but that was because my agent, who I’ve been with for decades now, suggested I raise limits. If I had not it would have gone down a little bit, too.

But that I had to up my coverage is evidence even in no man’s land Wyoming of Eric’s point. I had $50,000 in property coverage, which means if you are deemed at fault and it was a fully loaded Super Duty you wrecked the insurance would tap out at $50,000 and you are personally on the hook for the amount above that. Or if you’re in a multi-car accident even with sub-$50k cars but there’s perhaps three of them at $25k you get to pay for whatever the costs are above your limits. Even at $100k I look around and start to feel like no number is going to be enough.

Even within the insurance mafia the coverage is practically useless. My state minimum is $20k per accident for property (total of all cars), $25k per person for medical or $50k total per accident. You’ll be on the hook for a lot personally in a serious accident. So if you do choose the absolute minimum, even if you don’t to be honest, you need to structure your finances to protect assets or have a ton squirreled away for a good lawyer.

It’s a big problem, but the insurers aren’t raising rates solely because new cars are $50k and up. Certainly that is a major factor, but there are other factors.

If you buy insurance from a big national company that sells both homeowner and auto policies, you’re also paying for their losses on multimillion-dollar homes lost to hurricanes in Florida or wildfires in California.

Another factor is that there are now ambulance-chasing lawyers EVERYWHERE advertising every five minutes on radio and TV that you should hire them to sue for “slip and fall” and car accident claims. There are of course legitimate injuries that should be compensated, but we all know that personal injury law is also to a very large extent a fucking racket where the lawyers encourage questionable claims to see of they can shake a settlement out of you and your insurer rather than fight the case.

A few years ago I had $1 million in liability insurance on four vehicles for about $1900. The last renewal they wanted almost $4300. I shopped elsewhere and got a better deal, but it was still higher than it previously was.

Inflation is crazy. Everything has basically doubled in price within the past 5-10 years — houses, cars, groceries, etc. Your insurance has doubled, too.

For a few years now, I’ve been paying more for insurance on my family’s three vehicles than I’m paying for gas. Makes my blood boil.

Amen, ft –

AI’m personally near my line-in-the-sand moment. If the bastards increase my premium by a similar amount next year and I cannot find an alternative, I will seriously consider just “riding dirty.” I tire if being bled white by scumbags over harms I’ve not caused.

The problem is that you have a house and income and other assets. If you get into an accident and they pin the blame on you (deservedly or not, some of these can be subjective) your house and your Trans-Am are assets they can sue you for if you have no insurance. The Mexican illegals get away with it because they have no assets and nothing to take.

I hate paying insurance as much as anyone but I sure as hell would rather pay the insurance piper than lose everything I’ve worked for to some greedy lawyer representing a sleazy client faking a neck or back injury to loot my bank account.

No such thing as “accidents.” They’re acts of negligence. Eric has confidence in his ability to drive in a non-negligent manor. That’s probably his best bet in town.

If you’re relying on semantics in language when you argue in front of a judge you’re going to be screwed big time. The system is structured to bleed you dry if you don’t have a good lawyer and financial planner to get things into protected instruments like a family trust. You have been entered into a game you didn’t ask to play, will probably lose if you don’t play and can’t quit if you want to stay at all engaged. You can go rogue like an illegal or homeless but you will have to decide to walk away from what we know as a “good middle class” lifestyle in America. The alternative is to go off shore but the IRS constantly is tightening that noose so you can’t expatriate without penalty and soon it’ll be a forever social contract you’re bound to that you never signed.

Creative use of trusts can take care of that little problem.

Or — if you trust them enough — put everything in a close friend or family member’s name (note: if they get sued you get screwed)

You’ve been hoodwinked, duped, lied to, fished-in, you are the sucker being used for bait.

Drive an older vehicle, minimum coverage, high deductible, not comprehensive, not worth it, if the vehicle gets totaled, buy another beater.

Don’t have to own a vehicle, that will eliminate the cost of the insurance.

Dotgov will retain funds just by eliminating income taxes, no internal revenue service, dollars not spent, no tax accountants, no agents to hire, no special agents to carry a side-arm.

Not one IRS agent earns his keep, doesn’t earn a thing, collecting is the name of the game from the get go. No fleets of vehicles, winning.

Goes without saying that there will be more money for dotgov, not less. Or, less is always more.

No buildings to build, then maintain, no money paid to the gov, you get to keep what you do earn, voila, solved problems all over the place.

Uncle Sam would go mad, immediate delirium tremons, maybe anaphylaxis too. Jonesin for more money all of the time. Never satisfied, more, more, more.

The Vampire Squid won’t allow anything like that, therefore, let it rage on until it can’t anymore.

The gaping maw of the Vampire Squid voraciously devours everything.

Even on Sunday.

The daytime temps are not warm enough for gardens to sprout planted seeds, the Springtime temps are much cooler this year, looks like it from this vantage.

The wind is blowing 35 mph and the outside temperature is 52 degrees F.

My wife and I have liability coverage equal to our net worth. Plaintiff’s attorneys will go after the policy instead of our assets. We also have an umbrella policy which is supposed to cover liability for all manner of creative damage claims against us. We have an independent insurance agent, who finds us the best deals.

Insure the driver and insure the car separately. Since one can drive only one car at a time, this would make perfect sense.

Of course, the insurance companies don’t want to get rid of their handsomely rewarding “grift” by insuring each vehicle.

Money. I hate the stress and worry it causes people. The average American is economically illiterate. Knowing how to count money and even make decent money is nothing. How does someone make over $200k a year and only go deeper into debt? It’s not the making money part, it’s the spending part.

Have you seen those videos online where they train a pigeon or a raven to push a button when it hears a certain sound or sees a certain light, so that it can get food? It doesn’t take very long to have a fully trained bird. If only the bird could get out of the box.

The Bible teaches diligence, frugality, and charity.

“When they were filled, he said unto his disciples, Gather up the fragments that remain, that nothing be lost.” -John 6:12

Be frugal and never be wasteful. If you count pennies, you wont lose dollars very easily.

—-

“Thou oughtest therefore to have put my money to the exchangers, and then at my coming I should have received mine own with usury.” -Matthew 25:27

Invest what you can. It’s the very least of what’s expected. With $5k you can make $40-$250 a day with one or two trades. You’ll have to learn a bit. But those are hours you don’t have to work. Start with a strong and reliable company. One that’s not going anywhere soon. Buy when everyone else is panicking and the stock is low. Then, when it goes way back up, and everyone wants to buy it, that’s when you sell. If you buy it for $150, you don’t sell it at 149, or $110. Just hold. A person’s psychology messes them up more than anything in the market. Get your head right and don’t invest more than you can afford to lose, but don’t lose. Watch it for a month. Learn.

—-

And in Proverbs, the virtuous woman “She considereth a field, and buyeth it: with the fruit of her hands she planteth a vineyard.” -Proverbs 31:16

It doesn’t have to be the stock market. Buy flour, sell cake. Buy chickens, sell eggs. Pick up some extra side change.

—-

And regarding the law, but it conceptually works in economics all the same:

“So likewise ye, when ye shall have done all those things which are commanded you, say, We are unprofitable servants: we have done that which was our duty to do.” -Luke 17:10

A lot of folk need $10 so they make $10, and find they’re no better off. They merely bought their selves another day. Like fat, change your lifestyle and you won’t have to count so much. If you cut all carbs, get a little cardio, and only eat a really nice chicken salad until supper timer, well, that person doesn’t really need to count calories anymore.

You will find a balance that makes you happy and more financially secure and free. You just have to address it, which is something most people haven’t done or had the time to do because the system is designed to screw everyone. But it can be beat.

Do all this and you’ll very likely have enough to “Give to every man that asketh of thee; and of him that taketh away thy goods ask them not again.” -Luke 6:30

‘the federal government and even many state governments are NOT looking out for “the little guys”, but rather themselves and powerful, wealthy people and interests such as Big Tech, Big Pharma & the military-industrial complex.’ — JohnB

As one example, eighty years ago the US ‘forgot’ to demobilize from WW II, as it had from WW I. Ruling the world with its 800-plus overseas military bases bleeds off a steady 2-3% of GDP, which should have been invested in infrastructure and raising living standards.

The result is obvious: while the US stood still with its economic vitality being leeched away, a number of countries in Asia went from dire poverty to advanced economies in a couple of generations. Imagine if the US had kept advancing from its 1960s prosperity. Those flying cars they promised us by 1985 would be whizzing all over the skies.

Likewise, US health spending at 14% of GDP is about double that of other advanced countries, with poorer results (lower life expectancy). WTF?? That 7 percent rakeoff, compounded over decades, produced an underclass living in cars and RVs and cardboard boxes.

America stands for only one thing now: grift on a titanic scale. And the Orange Emperor’s Big, Butt-Ugly Bill will keep it that way. Like a gigantic, obdurate warthog, the Uniparty has a thick leathery face, and is incapable of feeling shame or remorse at it snarfs and slobbers at its filthy feeding trough of looted currency.

Jim,

There’s also the issue of the CDC adding all sorts of vaccines to the “Childhood vaccination schedule” (which many public schools diligently follow and require their students to have those vaxxes to attend) after a law was passed almost 40 years ago giving vaccine manufacturers immunity from being sued for injuries or deaths caused by their jabs.

There were people out there warning for years that there were efforts to create an “Adult vaccination schedule” and make it MANDATORY for adults to take certain vaccines, and as we saw during COVID hysteria, they were right.

Property taxes in Texas are already unaffordable, but the Legislature keeps the plates spinning by paying a portion of the “owners'” tax bills using state surplus money.

The “reform” scheme will continue for at least two more years, keeping voters unaware of being priced out of their homes until it is too late.

I once considered moving to Texas, somewhere around the Corpus Christi area. I thought the property taxes at the time were reasonably low. They were about the same as the area I contemplated moving from. The winters are nice.

They are no longer low. Haven’t been for a while. I moved to Houston in 2011. Prices for a modest house were under 150k. My price range was 125k or so. The taxes on a 125k home were around 2.5k. The same 125k home is worth 300k or so. Taxes are around 5k. There is nothing cheap about it. Yes, NJ and IL, places like that, are higher, but homeowners insurance is also a nightmare. On a 300k house, you are looking at almost 3k a year insurance.

House and Senate “Republicans” play a game every year where they increase property homestead tax “exemptions” in the “less taxes, lower government charade” It usually amounts to about $100 for the first year and then it goes up $150 the next year. The cycle plays out again.

Property values don’t go down a significant amount here due to a still robust economy.

there are signs of a tigtening, but I think we are 6 months out for the beginnings of a meaningful correction.

What it means, I don’t know, but Texas is a big government state except if you are rich corporate conglomerate. Then you can spread your concrete and gravel around after your bulldozers, backhoes and skip loaders have stripped every tree from the land. The place has been overrun by fast food eating establishments, big discount shopping strips, megadealerships, chain Mexican restaurant restaurants and billboards for decades. Houston TX is a monotonous droning concrete landscape.

The only reason I like it is that you can still move along at 80 mph on the freeway when traffic is freeflowing, generally unmolested by police, who are busy fighting real criminals.

Welcome to the end result of your service economy. Ship the value added manufacturing overseas, flood the labor market with cheap imported labor who also don’t adhere to “the law”, native USA citizens chasing their tail trying to get ahead financially. Corporations driven by quarterly stock goals. Government interference with the passive white population and lack of enforcement to all others. Check your state most wanted list, here in WA those aren’t Amish kids on there.

So, not enough manufacturing to build national wealth, service economy circling the drain as the dollar is worth less and less. The “services” cost more and more and then in the case of insurance $$$ turbo charged by the reckless behavior of the imported labor folks. Sparkey Downer but I just don’t see this getting fixed – too many facets of modern America need a hard reset.

“Check your state most wanted list, here in WA those aren’t Amish kids on there”

Same here. If a certain segment of the population were removed, crime would go down by at least 90%.

If the past 5 years have proven anything, it’s that the federal government and even many state governments are NOT looking out for “the little guys”, but rather themselves and powerful, wealthy people and interests such as Big Tech, Big Pharma & the military-industrial complex. Even the 2 major political parties have become corrupt. The Democratic Party is either f***ING insane or Swamp creatures, and the Republican Party has become either wimps or Swamp creatures themselves. Just look at the “Big Beautiful Bill”. Who the heck put a provision in it that says states can’t issue regulations regarding AI for 10 years? It’s almost as if someone wants to pass a law saying AI manufacturers can’t be sued for harms caused by AI. Where have we seen that before?

Mainly the “no state AI regs for 10 years” was to prevent California from setting the nationwide regulations. Congress can set regulations, but the insane CA legislature can’t mandate what the country does.

Hi Bob,

Even if that provision was to prevent California from setting nationwide regulations on AI, at this point there are too many unknowns with AI, and there are authoritarian governments and technocrats out there who would undoubtedly LOVE to use AI against ordinary citizens in one way or another.

They have also done in the auto industry the same thing as in medical care. I had a relatively small dent in my car where I bumped into a gate. I was not wanting to go to insurance to pay for it, I figured it may be about $1,000 to fix as it was not that big. I go around getting quotes and the smallest quote was $3,000. So they have gamed the system like they have for health insurance where you cannot do anything without them because it is an astronomical expense just to do something like have a routine visit to the doctor or fix a small dent in your car.

It is pretty obvious that owning and driving a car is becoming a kind of luxury – and luxuries are things most people cannot afford.

The whole idea of earning frequent flier miles (now “points”) to encourage loyalty to a particular airline is a big part of the problem. Now, instead of trying to save up FRNs for vacation, you just bank a bunch of points. Points can be used in lieu of money for many different expenses including food and drinks (or just earn more “points” to start building up the bank again). It is a form of selective deflation in a way because people who otherwise couldn’t go somewhere and are incapable of keeping what used to be called a Christmas club account to save up for a future event are now able to spend their way to a discount. But the cash price of travel continues to climb* instead of fall.

So what’s the point of being a rich f***er if everyone else can fly to the same exotic getaway, stay at the same hotel, eat at the same restaurant, enjoy the same views? Especially if you have to wait in line with the rest of the hoi-polloi? So better to make the daily grind more difficult for everyone else? And keep dangling out high tech solutions that will take even more of their monthly pay, but somehow don’t seem to be moving forward at a reasonable pace? Keep promising, keep ratcheting up the price. And eventually something will give -meaning the lines will be shorter, the traffic a little less congested, and life’s little struggles will go back to being fixed with a checkbook.

*Southwest is the latest casualty of the demand for returns. Now instead of doing a far better job than the rest of the industry and capitalizing on their loyalty, they’re just like everyone else, publishing a deceptive seat price and tacking on charges. Oh well. This is what happens when the psychopaths are let loose on Wall Street.

“ So what’s the point of being a rich f***er if everyone else can fly to the same exotic getaway, stay at the same hotel, eat at the same restaurant, enjoy the same views? “

Yep, “Mortimer, I noticed there were several ruffians on the links while I waited for my tee time!” So, time to pull the rug out from under the middle class with a nice steep recession.

Remember what happened to Mortimer and Randall.

Sadly, they rebuilt their fortune according to the script for “Coming 2 America”.

This is exactly what is happening and it entirely planned and intentional.

Insurance, parts, repairs and the price of vehicles have skyrocketed and Central Planners couldn’t be happier. Unfortunately most Americans are too stupid and lazy to see what is going on and beg to be lied to and manipulated.

Can’t afford to bet against yourself, which is exactly what all insurance is. Actually worse than that as regards car insurance, since the “law” requires you to bet against yourself.

Sadly, if people can’t afford a $500 emergency bill I don’t see how they can afford to insure their cars with these massive cost increases. As the economy gets worse a lot more people are going to be driving without insurance. Hopefully they will at least drive more carefully so as to avoid an accident but I’m not holding my breath waiting for that to happen.

Morning, Landru!

Yup. I feel myself being pushed toward this. The cost of the coverage I’m forced to buy has already doubled. It is still “only” $300 annually. But next year it may be $600. The year after, $1,000. My truck is worth maybe $3,500. I am not going to pay the equivalent of its value in “coverage” – just because other people want to drive $50,000-plus vehicles. Especially given I have not so much as scratched their paint. I think the time approaches to become a Gringo Me Gustan. They do it. Why can’t we?

Because a lawyer will hire a PI and discover what assets they can grab and you will be crewed, all costs on you. in Spain, driving without car insurance is a 3,000€ fine and loss of licence for about year.

Hi Pancho,

Yup. The answer is to become judgment-proof. No assets they can lay hands on. Just like the Me Gustans. Me gusta!

I’m in the process of buying one of my parent’s vehicles. The insurance agent highly recommended I increase the amount of “uninsured driver” coverage because they’re seeing more claims than there were 10+ years ago when I took out the policy. Anecdotal for sure, but it’s already happening.

That’s my favorite Catch-22 regarding auto insurance – it’s mandatory, so why would you need insurance against people who don’t have insurance?