Maybe being forced to buy health insurance will open people’s eyes about being forced to buy car insurance – mandatory car insurance being the trail run or Beta test for forcing us to buy health insurance.

It was imposed on the same pretexts: The government must make the buying of coverage mandatory because otherwise some people won’t buy it and those people “impose costs” on the ones who do. This would perhaps be sound if it were true but of course it’s false – on both counts.

On the first count, it is not debatable that there are people – probably millions of people – who are forced to buy coverage they never use because they never wreck.

Therefore, they impose costs on no one.

Such people nonetheless have costs imposed on them; are are made to pay for damages they haven’t caused. This is the same principle upon which Obamacare is founded. The healthy who incur no costs are made to hand over money to the insurance mafia for the benefit of those who do incur them.

And for the benefit of the insurance mafia itself.

Both mafias – car and health – profit enormously from being legally empowered to force people to buy their services. Socialized medicine is a moral outrage in the countries where it it is practiced, but at least it is not practiced for profit. Here, it is.

Car insurance at gunpoint, too.

It is dumbfounding that people complain about the cost of their “coverage” – both kinds – and yet do not lay the blame at the feet of thugs whose offers you can’t refuse. What do you suppose would happen to the cost of any other thing if the government decreed you had to buy it? And then made it legal – or at least, not illegal – for those purveying the service in question to make as much profit on the transaction as they could extort – which is exactly the correct word given you cannot say “no, thanks” without repercussions.

The ability to decline a service (or not buy a product) is the only check on what those of the left and sometimes the right sloppily refer to as profiteering. If you can say no – are not forced to say yes – then there can be no such thing as profiteering. There is merely the going rate – which you are free to pay or not.

This week, I am test driving a new Mercedes S63 AMG (review here). It costs nearly $200,000 but it costs me nothing because I can choose not to buy it. And the fact that others can choose not to buy it, too, means that if enough of those others also choose not to, Mercedes will have no choice but to lower the cost of the S63 AMG or not sell the thing at all.

In fact, Mercedes already has lowered it – or rather, is unable to charge more the car than the market will bear.

Profiteering, then, is just another way of saying: You are forced to pay whatever exorbitant rate is being charged, because you cannot decline without being punished. In the case of mandatory car and now health insurance, that punishment being monetary fines and even (potentially with Obamacare and actually with car insurance) threats of jail.

Regardless of your having harmed no one but merely because you failed to send the mafia the extortion payment demanded.

This, of course, is harmful to the mafia.

Back to the second pretext – this idea that without mandates-to-buy, there are people who will not buy. Of course, certainly. But this is a flatulent argument; smelly hot air.

The mandates haven’t altered that fact that there are still millions people who thumb their noses at the mandate and drive uninsured. If this were not a fact, why would it be necessary for most insurance policies to cover uninsured motorists?

All the mandate to carry insurance has done is to make insurance cost more for those who do carry it and the mass of those people are not the ones causing the trouble. But they’re forced to carry the costs of those who are – plus, of course, a tidy profit for the mafia.

And thus, it costs them more – including the ones who would buy coverage even if it were not mandated. They’d just pay less for it in that case. Which of course means less profit for the mafia – and that is the true reason for the mandate. It is an imbecility to believe otherwise.

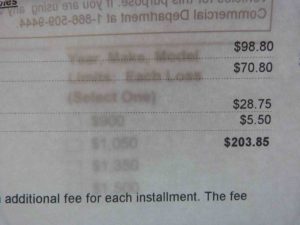

I got to thinking about all of this the other day, when my renewal – or else – notice came in the mail. The extortion letter demands $203.85 for the next six months to “cover” my 16-year-old truck (and my driving of it) neither of which have ever cost the mafia or anyone else a cent. Because I have never caused anyone any harm with my truck or my driving.

But the “coverage” has cost me more than the cost of the truck.

Well, it has cost me more than half what I paid for the truck, which was $7,500 about ten years ago. My annual premium-at-gunpoint is a bit more than $400 so that times ten is a bit more than $4,000 so far. I am well past the halfway mark toward paying more on insurance for the truck than I paid to buy the truck.

If that is not usurious then the word has no meaning.

It is actually usury via extortion – a double hit.

If I could say no – if that threat existed – the cost of my policy would have to be less because otherwise I would cancel it. That is called an incentive, in economics. I would be a customer, once again – one who must be pleased or he will take his business elsewhere.

The “or else” would be mine to wield – rather than the mafia’s.

But instead of violence – the mafia’s tool – economics.

Offer me reasonably priced coverage based on decades of accident-free driving and never having had a claim filed against me and I would probably buy a policy which would pay out in the the extremely unlikely event my driving causes harm to someone else or their property. I am not interested in covering my truck or even myself. The truck is old and I’m more than willing to assume the extremely low risk I may hurt myself in exchange for the certainty of not throwing away money I need for other things.

I think $100 a year is about right to “cover” a 16-year-old truck driven by a middle aged guy with decades of objectively responsible (because accident and claim-free) driving as the basis for rating my risk profile.

But a sum equivalent – so far – to more than half the priced I paid for my truck is by definition unreasonable. It is involuntary loan sharkery.

And my policy cost is relatively modest in the context of what many people pay, which is around twice what I pay, on average.

Part of the cost relates to the replacement cost of the insured vehicle; the nicer/newer the model, the higher that cost. Mine is old – yours may be newer. But what if you never need to replace it because you never wreck it? The money is gone, nonetheless – based on a theoretical loss never incurred.

This would be a morally acceptable transaction if the insured bought the coverage – and paid the price – willingly. But it’s a holdup when the victim has no choice; when it is pay up – or else.

Observe that there’s no refund given at the end of the term when the theoretical loss never materializes and meanwhile – because of the responsible conduct of the insured-at-gunpoint – the quarterly profits of the mafia increase by 20 percent.

The concept of insurance isn’t evil. It is made evil by making it mandatory. And it is made even more evil when it is made mandatory for the sake of profit.

. . .

Got a question about cars – or anything else? Click on the “ask Eric” link and send ’em in!

If you like what you’ve found here, please consider supporting EPautos.

We depend on you to keep the wheels turning!

Our donate button is here.

If you prefer not to use PayPal, our mailing address is:

EPautos

721 Hummingbird Lane SE

Copper Hill, VA 24079

PS: EPautos magnets are free to those who send in $20 or more. My latest eBook is also available for your favorite price – free! Click here. If you find it useful, consider contributing a couple of bucks!

Lie")

{kind=link}

Americans should understand that they are slaves now.

The US is an immoral bankrupt warmongering police state.

Why obey the law if the government and illegal immigrants don’t?

Everything is fake and a lie now.

You can either:

Work hard to pay taxes that fund welfare, illegal aliens, tyranny, wars, and debt and live with regret when the US Ponzi collapses and Americans get sent to the concentration camps.

OR

Be dependent on welfare.

OR

Break the law working off the books.

OR

Waste your life trying to warn people of the dangers of war, debt, and tyranny.

“but at least it is not practiced for profit”

There is always profit. Government just means the monetary profit is in the form of high paying, high benefits government jobs. Contracts for the right people too.

Auto insurance varies widely depending on the state. The regulatory structure and competition. The people’s republic of Illinois has pretty low auto insurance rates. Illinois allows outfits like “The General” and “Eagle” insurance to operate which results in heavier price competition despite the mandate.

https://www.youtube.com/watch?v=ogh8E4eYhV0

I have found that many “non”-profits are far worse when it comes how they money is used.

ugh, my grammar! Many non profits are far worse then a for profit, to how they manage the “profit”. One of the reasons why I will likely never give my alma mater any money, they waste so much of it, its criminal.

Agree Brent and Rich,

Here in the UK the sheep spent all of last week worshiping the arm of the state called the NHS as it was its 70th birthday. The reality is they have no idea how crappy it is relative to how much is put into it. I read somewhere the difference between capitalism and socialism is who makes the profit. Here the NHS is charged like 20 pounds for say a pair of disposable gloves, 500 pounds to change a light bulb…. Or the PFI contracts where the government gave companies land and a ton of money to build a hospital then leased them back for the NHS on 50 year or so contracts at exorbitant amounts (say the cost of the hospital was repaid in a couple years)….. Someone IS making a ton of profit, and in a more consistent and insulated from the end client way…. whats worse here whenever you try to complain at the shitty service they look at you as some ungrateful bastard who is not thankful enough at the “free” healthcare you are getting….. And even if it gets heard the doctor blames a nurse who blames a contractor who cant do more because its his job and a union contract doesnt allow him…. the story goes on…. there is absolutely ZERO concept of accountability…..

The reason most people dont realise is its paid for by the state via higher (and constantly increasing) taxes and unlimited borrowing (they dont have any borrowing cap like they do in the US). Then suddenly when the country goes the way of Greece or Italy, they wonder why…….

Michigan has the highest automobile insurance premiums in the country due to the “unlimited medical claims” system that is mandated by state law. That is not the whole picture, as health care providers purposely charge more for automobile-accident related medical services. The “Michigan Catastrophic Claims Association” (MCCA) is the quasi-governmental organization that pays the medical portion of automotive accident claims only when insurance maximums are exceeded and has hundreds of billions (yes, hundreds of billions of dollars that it is sitting on) of dollars in its coffers.

Each vehicle insured is charged an amount on top of the insurance premiums, despite the MCCA being flush with cash and not paying much out in claims. The current assessment is $192.00 per vehicle…that is on top of the normal insurance charge.

If I had my way, auto insurance would be underwritten to individuals, not cars. Since a person can only drive one car at a time, it makes sense to have auto insurance tied to the driver, not to the vehicle.

I’ve long stated that auto insurance, at the very least liability, should be per person because a person can only operate one vehicle at a time. But then I realized the game being played, it was to penalize people with more than one vehicle under the idea that the car may be loaned to someone without insurance. But if insurance is mandatory then just tie to the DL. Much easier for the state to enforce buying the product too. But again its not about logic it is about penalizing multiple vehicle ownership, ownership of sports cars, etc and so on.

I’m also in the bucket of zero accidents on my record. Paying $1700 a year for a 13′ and 11′ model truck and SUV. I’ve had a bunch of claims against the truck. Insurance co. actually bailed me out in a hit and run where Houston PD told me to pound sand. Caught the license plate, HPD said meh we are too busy, Insurance gave me the name and address of the guy and I did some googling and found he worked at the same company I do. Ended up getting him to pay for damages. Gate arm at work closed on the truck also denting the hood. Had to file workers comp of all things to get coverage, a brand new hood! Lady I gave my deposition too (Texas State Workers Comp person) asked me how fast I was driving when the accident occurred, she choked when I said zero miles an hour. Other than that, $1700 could be invested in a savings account as both are vehicles are accident and incident free.