A few weeks back, I wrote a column about the mafia tactics of the insurance . . . mafia. Which I refer to as such because it works almost exactly like the families portrayed in Mario Puzo’s Godfather series. They “make you an offer you can’t refuse” – regarding “protection” which you’d better pay for, if you know what’s good for you.

The main difference between this legal mafia and the not-legal mafia is that the insurance mafia uses the government to make you an offer you can’t refuse – the “protection” offered being mandated by law.

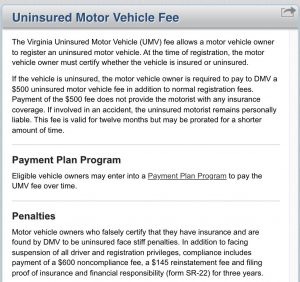

My state, Virginia, generously allows people to not pay the mafia by paying the government instead – with the additional downside of no “protection” in return for the annually due $500 Uninsured Motorist Fee. Payment allows you to drive without insurance legally – an interesting thing in view of the government’s feigned attitude toward people who drive without insurance. The risk to other drivers apparently isn’t the issue. The paying of money, is.

Especially if you don’t pay it. The fines – and penalties – for that are serious.

Anyhow, I’d been paying GEICO for going on 20 years. During all the time I’ve been with GEICO I’d never filed a claim nor had one filed against me. In other words, I have cost GEICO nothing – but have paid them a lot. I probably would have continued to pay them – had they not tried to squeeze me one more time.

When I got my latest policy renewal, I noticed a substantial increase in the cost of my coverage. It jumped from about $170 for six months to more than $190. This puzzled me, initially, because I knew I had not filed any claims nor had any filed against me; had not even had a seatbelt ticket they could use as a pretext against me. Also, the vehicle I had covered with them is my 2002 Nissan pick-up, not exactly a heavy liability potential there.

So I called to try to find out what was up and felt pretty confident some kind of mistake had been made or – at least – some accommodation could be made. I figured I was in a strong position because I am probably the perfect “customer” – if such a word can be used in any context where you’re forced to be a “customer.” I’m a middle-aged guy with no kids and an accident-free record going back decades. I’ve established that I’m extremely unlikely to cost them anything – ever.

Meanwhile they’re making book on me.

How much book?

The wanted just shy of $200 for six months – about $400 annually. This is what GEICO thinks is a reasonable sum to charge for a state-minimum, liability-only policy on a 20-year-old truck driven by a guy who has never filed a claim or cost them a cent in loss.

Were I to continue paying this I’d have lost a sum equivalent to the current fair market value of my truck in not too-many-years-from-now. This is not counting what I have already paid GEICO for this “coverage,” which is roughly in the ballpark of $5,100 – more than what my truck is worth right now. Add ’em both together and I could buy myself a new (used) truck.

It begins to chafe – and so, I called.

The woman I got told me the increase was due to my state raising the mandatory minimum coverage amounts it forces all car owners to buy – unless of course they hand over that $500 “fee” to the government to be granted the privilege to drive around with no coverage whatsoever – leaving you liable for whatever damage you do to someone else’s property. As it should be in all cases, by the way. But it gives the lie to this line about government imposing coverage requirements so as to deal with the “problem” of people driving around without insurance.

Spare me.

I replied that this was of no relevance in my case because I’ve not filed a claim nor had one filed against me; my record of claim-free driving going back decades, on the other hand, is relevant. I added that while the proposed premium hike wasn’t huge, I found it obnoxious in principle and expected it to be removed. She would not budge. It didn’t matter that I’d not given any reason to believe I would be costing them any money – as opposed to being expected to pay them more of it. The new premium wasn’t negotiable. And it’s due in two weeks (early February).

I told her I’d be shopping around – which didn’t faze her, either. Now I’m glad it didn’t.

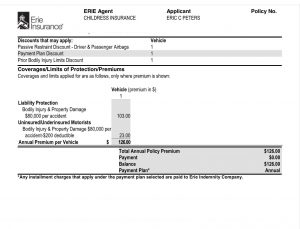

As it turned out, I was able to buy exactly the same coverage from another company – technically, via an insurance broker – for less than half what GEICO was extorting from me. This is a policy I would have freely bought, had I been aware of it, because the cost of the coverage – state liability minimums – was low enough to justify paying it. While I judge my risk of being at-fault in an accident (or even having an accident, at all) to be slim-to-nil (backed up by my decades of accident-free driving) there is always that chance and paying $126 or so per year for just-in-case seems . . . reasonable to me.

I’m not spending almost as much on “coverage” as my truck is worth.

It was wonderful to get the increasingly desperate-sounding mail (and email) from GEICO, wondering why I had not sent them any money. I just called to tell them why, exactly. All of a sudden, they wanted to talk. But I no longer did.

I still don’t like being made to be anyone’s “customer.” But I can vouch for the fact that it pays to shop around – and in particular, to talk with an insurance broker rather than just one insurance company. There is still the element of coercion, but there’s also enough competition for your “business” to make a difference.

. . .

Got a question about cars, bikes, or Sickness Psychosis? Click on the “ask Eric” link and send ’em in! Or email me at EPeters952@yahoo.com if the @!** “ask Eric” button doesn’t work!

If you like what you’ve found here please consider supporting EPautos.

We depend on you to keep the wheels turning!

Our donate button is here.

If you prefer not to use PayPal, our mailing address is:

EPautos

721 Hummingbird Lane SE

Copper Hill, VA 24079

PS: Get an EPautos magnet or sticker or coaster in return for a $20 or more one-time donation or a $10 or more monthly recurring donation. (Please be sure to tell us you want a magnet or sticker or coaster – and also, provide an address, so we know where to mail the thing!)

My eBook about car buying (new and used) is also available for your favorite price – free! Click here. If that fails, email me at EPeters952@yahoo.com and I will send you a copy directly!

{kind=link}

GEICO is owned by Warren Buffett, no friend to the common man nor America; Progressive is owned by George Soros, avowed enemy of the common man and America. Shop for small, non-hedge-fund-owned companies.

GIECO is also one of the more expensive co.s- but their advertising BS seems to have convinced many people that they are a bargain……

Had been with Geico for 9 1/2 years when I switched to State Farm a few months ago. Upon calling Geico to cancel my policy, they asked if there was anything they could do to keep me.

I said, “Sure, lower your rate. It keeps increasing and has become unaffordable.”

I own two 2007 Hondas and have a teenager on my insurance. Both have full coverage. My monthly rate was around $179. We had no accidents or traffic tickets.

The response from GEICO was to tell me to lower my liability coverage, which I won’t do.

I said, “Well, it comes down to dollars and cents and you’re costing me too much money.”

You’re right, Eric. They don’t give a damn.

Hi Jim,

I just had the pleasure of formally telling GEICO they’d lost me as a customer. It was worth going through the phone tree. I told the woman, when she asked why I was not renewing, that I got tired of being screwed. That their recent attempt to snatch another $40 out of my pocket for no legitimate reason (spare me about the state increasing its mandatory minimums; this doesn’t cost GEICO a cent if I don’t file a claim and I have never filed one in some 20 years of being a customer) was the final straw and that I hoped they understand how much money they just lost by trying to screw me out of some more.

If anyone’s interested, Erie seems ok based on my experience. Almost not a mafia, even!

Eric, the insurance crime mob is legalized theft, enforced by government stronger mandates. The real dilemma for us proles is how do we go about

minimizing the tribute extorted from our meager pockets into theirs? Unfortunately, calling around and comparing rates, either yearly or every other year is the best method to keep the theft to the minimum. The reason is that when the State insurance Commissioner (commizar) approves a new company to do business in your state, he will also allow the newly approved company to deviate from accepted rates approved by the insurance Commissioner by up to 40 and even 50% off what other companies are charging customer at right now. It’s a complete racket. Your rates will increase.

You’re right, of course – as regards “your rates will increase.” This being inevitable when they know you have to buy coverage. I suspect, however, that as their insolence increases, more and people will just go pirate and drive without “coverage.” If it’s good enough for illegals, it’s good enough for us!

I was just reminded about another “mafia” sort of extortion thing! Not insurance related but I see that I have the tax form from the state that lists last years refund as taxable income!

What in effing hell is that?!?! First, they stole more money than they felt was necessary, but all the previous years income was, in fact, already taxed.

But now the money that I already earned, that they confiscated and returned, I get to pay tax on once again?!?!

God dammit these people freaking insane.

Is that what this 1099-G form is all about?

Yes, but it isn’t always taxable. If you take the standard deduction your previous year state refund is not taxable. Also, if you are someone that qualifies for itemized deductions (Schedule A), but are capped at the $10K for RE taxes, personal property, and state income taxes then only a portion or maybe zero of the refund is taxable.

If you move to a state that has no state income taxes then this isn’t even an issue. 😉

I live in a state a long way from VA. Recently my rate went up as well, for no apparent reason. Only a few dollars though. I chocked it up to inflation.

Another scam insurance, though not mandated (AFAIK), is dental insurance. This is provided by my employer along with (but separate from) the mandatory medical insurance. They are supposed to pay for one teeth cleaning a year and cover some percentage of typical dental procedures.

Well, I went to my periodontist (as I have been doing for the past 7 years or more) and had them clean my teeth a couple weeks ago. It was a typical teeth cleaning the same as I’ve always had my entire life.

But the dental insurance won’t pay for it. You see the practice (being periodontal) uses a “periodontal cleaning” code and they refuse to use any different code even though it’s the same damn cleaning as any dentist would do. And the insurance company says they won’t pay for it unless there was some *other* periodontal procedure done in the last two years.

I’ve got gum issues, so I get 3 – 4 of these cleanings per year at this periodontist. I choose them because they provide the very hard to find “laser prophy” procedure if it becomes necessary. Nobody else in the area does that.

So I *have* had other “periodontal procedures” in the last two years (actually within the last few months) paid for 100% by me but somehow that doesn’t count. The practice even resubmitted, and I called the insurance company but basically the answer is the same: GFY.

Lastly, how in hell is the health/disease condition of my mouth not “medical” in the first place? I’m telling you man, all this medical/dental insurance is a major scam. Just as bad or worse as auto insurance.

The Fundamental Medical Scam is “we don’t promise to do anything except take your money.” “Procedure” didn’t work? TS, chump. You owe us anyway. Full price, no discount for failure to provide anything of value.

The Fundamental Medical Insurance Scam is “you don’t get to know how much it costs, or whether so-called ‘insurance’ will pay for it, until after the deed has been done.” “Insurance” didn’t pay? TS, chump. you owe us now. Can’t pay? Hope you enjoy the rest of your life, in a cardboard box, in some homeless camp.

A real racket, if you can get away with it.

RICO should apply, IMO.

But if you own your very own U.S. Senator:

https://en.wikipedia.org/wiki/Thomas_F._Frist_Jr.

many things become possible.

I feel your pain, EM –

It’s why I just pay out of pocket for my annual cleaning/whatever work I need. Much less hassle and – interestingly – cost. It’s about $75 to get my teeth cleaned; I had to have a cavity filled last year; about $150. Two years ago, I paid out of pocket for a crown, about $1,200. How much would a “policy” for a year cost? I’m guessing a lot more – plus the hassle.

Eric,

I have 1Dental, a discount plan. It easily pays for itself. I had dental insurance awhile back and, you’re right, out of pocket is cheaper.

>paying $126 or so per year for just-in-case seems . . . reasonable to me.

Except you will quickly blow through your policy limit if you should ever get in a wreck & be held liable. $80,000 *might* cover p.d. if you total a high end vehicle. B.I.? Now we are talking doctors & hospitals. If you think insurance companies are bad, wait until you (or your insurance co.) comes face to face with Guido the hospital capo. No normal human being can afford to pay these criminals, which is what they are.

And that’s just liability coverage, Eric. Suppose some clover puts you and one of your bikes in the weeds. You may be the safest driver in he world, but you have *NO* control over the idiots (who should not be) on the road. *IF* you are still breathing, the body snatchers (“ambulance”) will transport you, quite possibly unconscious, to the bank of the river Styx (entrance to “hospital”). Once you cross that threshold, the line from Dante’s Inferno applies: “abandon hope, all ye who enter here,” particularly as regards your finances.

They will charge outrageous fees, and *LIE* about justification for “tests” you do not need. BTDT in 2014. At that time, $34,000 to roll me, unconscious (therefore without my consent) through the front door. I foolishly signed the consent form upon regaining consciousness. Never again. Routine blood tests, which might cost $200 at your local medical lab? Nine *THOUSAND* U.S. dollars. CT scan, including lying about “reason” for test? $10,000 per scan, times five scans.

Bottom line: 18 hours at Riverside Criminal Hospital exceeded $100,000, which is my automobile medical limit (maximum State Farm will write, for that risk). I was on the hook for several thousand, for an accident in which my most serious “injury” was a mild concussion, complete with retrograde amnesia, caused by the air bag striking me in the face. Also, about six drops of blood from my nose.

My suggestion? If you ever find yourself in a “hospital,” run, walk, or crawl to the nearest exit. DO NOT, under any circumstances, sign any form which “authorizes” the “hospital” to “provide medical treatment.”

Oh, and be sure not to own property in your own name. An attorney who specializes in asset protection can help you with this, if you have not already done so. Ask around, and pay a well regarded specialist (not Jimmy McGill!) his (reasonable) fee. This will probably involve a trust, which should make you appear poor, on the face of it, and thus a poor target for a lawsuit.

JMO, and IANAL.

BOL, Eric. I do *not* want to hear that you are homeless, and writing your prose on a laptop from the local public library, which you *might* be allowed into if you wear the hated, filthy face diaper. Just sayin’… 🙂

> a high end vehicle.

By that I mean to say, “someone else’s high end vehicle” (p.d. liability). These days, it doesn’t take all that much to total a vehicle, what with all the “high tech” gizmos (dealer items!). It is quite possible to walk away from a wreck, and find your ride, or the other guy’s ride, or both, are not economical to repair. Which might be a blessing, because it means you will not be driving a patched up heap, but you ,or your insurance co, will be on the hook for replacement cost. Be prepared to fight for it, if it is your own vehicle.

Here’s a hint. If you buy or lease a new auto, save the window sticker. Should the time come to settle up, you have proof of how the car was equipped. Big difference, these days, between the “basic” setup and a “high end” package on the same model. If you have the sticker, the insurance co cannot shuck & jive for very long. It worked for me.

>idiots (who should not be) on the road.

One such idiot crossed over the turn lane into opposing traffic and offed himself on my front bumper back in 1989. Totaled himself, his county issue Kawasaki, and my ’85 Ford Ranger. I estimate the relative velocity at time of collision to be less than 50mph. There were long skid marks on the pavement from both vehicles.

I was not physically injured, but I learned the meaning of the term “post traumatic stress syndrome.” NF, and not recommended.

Allstate, my insurer, paid me promptly, and fought it out with County of Riverside for the harm caused by their employee, who in my opinion was poorly trained.

Some time before that, I had attended a safety seminar (“lunch & learn”) given by a CHP motorcycle officer. He stated that, in any head on collision, CHP expects at least one fatality. He also stated that CHP puts 5% of its miles on motorcycles, but experiences 95% of serious injuries on motorcycles.

My brother once owned a Kawasaki Z1B, which at the time was touted as “the world’s fastest production motorcycle.” It was fast. My brother is one of the safest drivers I know, but some idiot cut him off, and he had to lay the bike down, thus demonstrating the old adage about there being “two kinds of bikers, those who have been down, and those who will go down.” Fortunately for him, the wreck occurred at very low speed, and he walked away from it with only minor injuries. YMMV.

I hear you Turtle –

I know such things are possible. And your suggestion regarding asset protection is sensible. That said, I’m someone who believes that insurance – the whole works – is one of the chief reasons why so many people have so little money. I realized this at a young age and acted accordingly. I never bought health insurance. I often drove without car insurance (when I was in my young 20s). I spent next to nothing on insurance. Which left me with a lot more money than my friends who bought it.

I once added up everything I’d paid in for car/bike insurance “coverage” so far – since I was a teenager to now. It’s a lot of money – money just out the window, too. And I paid less than most people – and nothing for health insurance, which I want nothing to do with. People who do pay it are often spending a fourth or more of their income on this “coverage.” Plus “coverage” for their home (another gyp) and life, etc.

I’d rather run the slight risk and accept the certain benefit of having my money in pocket rather than theirs.

Hi, Eric,

>I never bought health insurance.

Neither have I.

First of all, “health” insurance is a misnomer.

If you are lucky, it *MIGHT* protect you from the depredations of the medical-industrial complex. Then again, maybe not. It will do nothing to “protect” your health, for which you are responsible (as you are fond of pointing out, and I agree). For “believers” (doctor worshippers), knock yourself out. For me, I will prefer to die in the woods, with sunshine and birds chirping, for free, when my time comes, rather than a “hospital,” with machines chirping and the smell of death all around, at a cost of several million dollars. Friend locally said it cost $3,000,000 for his dad to die in a hospital. I would prefer to leave something to my designated heirs, rather than donate my meager estate, plus a bundle, to the Church of Heap Strong Medicine, Kemo Sabe.

We all have to make our own cost-benefit assessments. I carry no life insurance, because I have no one to protect. Others may have a different situation.

Like most people in Calif, I carry no earthquake insurance, because it is expen$$$ive, and has 10% deductible. I do have standard homeowner’s policy (property still encumbered, due to improvements). I once knew an architect who cancelled his homeowner’s policy once he paid off the VA loan. Next winter was very wet one, and his house in Rim Forest ended up down the hill. Total loss. House free & clear, no insurance. Oh, well.

Jedem das seine, mein Herr.

Okay, this has nothing to do with insuring autos, but everything to do with insuring freedom. As our MSM does their best to hide what is occurring across the country of our Northern neighbor. A full fledged grass roots revolution. Mr. Trudeau is a man cornered. He has two choices: End the mandates or starve his people. Fifty thousand trucks and hundreds of thousands of Canadians are not caving.

https://www.youtube.com/watch?v=N23pYH18xGs

It does my little Aquarian heart proud. ❤️ Hopefully, this will be arriving at a city near us all. Go Canada!

Right now it appears that Mr. Trudeau bravely ran away…

Perhaps he thinks Herr Schwab will save him?

Perhaps Canada will learn that they can get along perfectly well without a Prime Minister?

What a freaking wuss. Instead of being a leader and meeting with his constituents to discuss their differences and arrive at a compromise he turns tail and hides. I would feel embarrassment for the Canadians, but we then I look at the weak old man who is occupying the White House and realize their leader can actually read a teleprompter and can tell the difference between his wife and sister.

I hope the Canadian truckers hold siege in Ottawa until Trudeau has no recourse but to overturn the mandates.

Hi RG,

If all of this were motivated by good intentions I would wonder with you. But it’s not. This has been a power grab from the beginning and people like Trudeau imagine themselves to be the leaders of the new order, a world run by a technocratic-managerial elite that organizes and controls essentially everything – with the populace reduced to being given the “choice” to obey or face the consequences of disobedience.

Hi Eric,

People can say I am naive, but this feels different. Courage is contagious. I believe this is the start of the Great Awakening. Of course, it will be years before we see the end results, but history has taught us that the elite are weak against the people when the people feel they have been deceived.

What did Hitler do? Did he hold his head high and take his punishment like a man? No, he hid in a bunker and when the Allied Forces showed up on his doorstep he shot himself like a coward would. Mussolini…strung up for the world to see, Robespierre and Ceausescu executed, Gaddafi found hidden in a storm drain, etc.

History has not been kind to those who have ruined the lives of others.

I still believe the Rockefeller Foundation’s “Scenarios for the Future of Technology” is a playbook and not a wish list. The WEF will never get “You will own nothing and be happy.” Pessimists will allude that I am wrong and my thoughts are wishful thinking and gullibility. Maybe. Bbut I believe the Earth and her people still have a little fight left. It just takes a lot to rouse them from sleep.

RG – Do you mean you’re hoping for President Biber to shoot himself in the head in whatever hole he is hiding in?? How could you !!?

On a separate note – the media saying it’s “the russians, the russians !”

Actually, I do not wish death or anyone except bad people. I arbor no ill will against Uncle Joe, because I realize he is a senile old man who cannot comprehend what he is doing or where he is at. I blame his family (and the American public that voted for him) for allowing him the ability to be a puppeteer and holding the nuclear codes. Instead of starting shit with Russia and Ukraine, scolding Americans for not getting the jab, and overseeing the highest increase of inflation in the last 40 years he really should be biding his time at home playing fetch with the dogs, enjoying his grandchildren, and taking daily walks.

Instead, our country has become a laughingstock and is viewed as weak because that is what our leadership is. The sad thing is there are 31% of Americans who still believe he is doing a good job. 🙁

>Instead, our country has become a laughingstock and is viewed as weak because that is what our leadership is.

Hear, hear.

>Gaddafi found hidden

Saddam Hussein, great admirer of J. Stalin, found hiding in a “spider hole.” Two sons, evil bastards though they were, had the courage to shoot it out, knowing they would be killed.

>Hitler….hid in a bunker and when the Allied Forces showed up on his doorstep he shot himself

Would it have been more “manly” to allow himself to be hanged? I am no admirer of Hitler, but I do believe he took the honorable way out, under the circumstances. (I know of an instance where someone shot himself in the heart rather than be arrested, and convicted for child molestation. Would it have been more “noble” for him to surrender to law enforcement? I think not, but you may have another opinion.)

>The WEF will never get “You will own nothing and be happy.”

LET’S HOPE NOT. 🙂

“Would it have been more “manly” to allow himself to be hanged?”

Actually, yes, it would have. I am a believer of “do the crime, do the time.” Hitler took millions of lives. That he feared for his own and took the sissy way out isn’t honorable. Every German, Hungarian, Russian, and Austrian citizen that was killed their family had a right to closure and if that closure was dangling in the Village Square, so be it. Personally, I think they should have put him on a train and allowed him a shower then dangled him in the Village Square, but that is just me.

If these dictators believe they are on the right side of history, stand by your principles! Don’t turn tail and run hoping that those whose lives you have destroyed now want your head. Fight! Instead, most of them sneak out in the middle of the night like a thief hoping some other country offers them hospitality for the hell that they put others through.

>Hitler took millions of lives.

Adolph Hitler himself took no lives. People *working* for him took millions of lives, a large number without just cause. A distinction without a difference? I think not.

He brought Germany to ruin by his “leadership,” that is for sure. But, he did not do that by himself. Great orator, terrible leader. Personally, I think the expressions “half a bubble off,” “a few bricks short of a load,” or “not playing with a full deck” describe him rather well. Quite intelligent, but not quite sane. He had some strange ideas, but people followed him. I guess that is called “charisma.”

>the sissy way out

I doubt he saw it that way. Putting a pistol to his head was equivalent to the ancient practice of falling on one’s sword, or the Japanese seppuku:

https://en.wikipedia.org/wiki/Seppuku

>As a samurai practice, seppuku was used voluntarily by samurai to die with honor rather than fall into the hands of their enemies

You might reasonably argue that it would have been nobler for him to die on the barricades, as he commanded others to do, and with that I would agree. But, he did not run away. He died in his own headquarters, by his own hand.

By contrast, I give you the despicable end of AH’s Number One Toady, one Heinrich Himmler, who *did* run away, and attempted to hide out, without success.

Personally, I believe some of the more, shall we say, “creative” medieval methods of execution, to involve great pain as well as great humiliation, would have been too good for Heinie. Too bad he managed to swallow cyanide.

Hi Turtle,

Lots of stuff about Hitler. Evil as he was, he wasn’t a physical coward – either as a young man or at the end. He was a dispatch runner in WWI – a hugely dangerous gig; he was awarded the Iron Cross, first class, for bravery – and deserved it. Very few – almost no – mere corporals were so decorated. An intuitive political genius who let his own arrogance blind himself to his many weaknesses, perhaps the chief of which was being unwilling to defer to skilled professional officers who might have won the war for him (Stalin was like Hitler at first, but was smart enough to realize his mistake and leave it to Zhukov and others to win the war).

As far as Hitler’s suicide: By 1945, he was a physically broken old man, not capable of fighting. But he stood his ground in the ruins of his capital city, refusing to flee – as a coward might have – when given (many) opportunities to do so.

hi, Eric,

Yes, everything you said, and more.

AH (& HG) were genuine war heroes from WWI.

AH awarded:

Iron Cross 1st class

Iron Cross 2nd class

Wound badge

(wounded by shrapnel as well as gassed)

In U.S. terms, this would probably translate to:

Silver Star

Bronze Star

Purple Heart

(I don’t know British equivalents – maybe someone here can help out.)

An Austrian citizen, he volunteered for the German army.

After the war, he could (and did) legitimately say, “I was there. Where were you?”

Unfortunately, we have been presented with what I call a “cartoon” version of Adolph Hitler, as well as many other things, which sheds no light on the history of Europe, or the World, from 1900-1945.

Fortunately, due to the “magic” of the Internet, it is now becoming much easier, for those with some natural curiosity, to dig a bit deeper. Unfortunately, probably very few wish to do so.

Henry Ford said, “Thinking is the hardest work there is, which is probably the reason so few engage in it.”

Hi RG,

Hitler was many vile things but I don’t think it’s possible to accuse him of cowardice. He was begged by several of his lackeys to flee Berlin – and Russian justice – while it was still possible. He refused – while giving permission for those around him to go, if they wished. It is understandable that he did not want to fall into his enemies’ hands. But he didn’t run away from them, either.

The ones who embarrassed themselves at the end were people like Himmler, Ribbentrop and Frank. Goring, on the other hand, went out like a lion. Bastard that he was, I respect him as a man – because he was one. Same as regards Rudolf Hess.

Several years ago, the History Channel, a cable network ran a series called “Hunting Hitler”. Being somewhat interested in history, I saw the entirety of the series, and, afterwards was left with serious doubts as to whether Hitler actually did commit suicide. I know that in the modern view of the Nazis, they’re dismissed a so many goose-stepping idiots, but, in fact, they were a formidable and ruthless adversary that came very close to winning WW2. The series left one with the impression that Hitler lived in protected seclusion in South America until his death in the early 1960’s. The US Government has a long history of lying to the people – why should we believe their assertion that Hitler committed suicide in the Fuhrer Bunker?

Did Osama bin Ladin die in a raid? Or did the CIA just bring him home? Like Hitler, we never got to see the bullet holes like we did with Kennedy.

Isn’t that the long and short of it? This piece of shit runs and hides like the little pussy he is. They all do. They all smugly thumb their nose at us, as they sit there fully insulated from the bullshit they promulgate. Like all bullies, they are cowards through and through. They won’t listen until there is a consequence.

>Like all bullies, they are cowards

You nailed it, BAC.

This is it exactly, BAC

Bullies – and something worse. No compassion or empathy at all for the evil they visit on others. I can see being carried away by the initial fear of the “plague.” What I cannot excuse is the ongoing of use of fear to maintain it.

You know what they (used to) say:

Lead, Follow, or Get Out of the Way!

Australia, Brazil, and Bolivia have similar convoys going on.

Do not buy any kind of insurance from a company agent. Or on line with no agent, which means the insurance company sticks the agent commission in its pocket while it charges you about the same as if you had an agent. Your loyalty is misplaced, as Eric discovered. It’s an independent agent’s, or broker’s job to find you the best product at the lowest price, and they have a lot of incentive to do so. And the flexibility to do it. Their commissions are high. Higher than you would suspect, and the company sets them. The agent, independent or not, cannot forgo commission to lower your price.

Plus, spending hours on the phone with an independent agent is not typical. The more customers they keep the more money they make.

Years ago I got hit by an uninsured driver. State Farm raised my rates. I dropped them and went to usaa. That was my only fender bender in 40 years of driving.

Wow that is incredibly cheap. Miami is the insurance fraud capital of the US with horrible traffic and I know someone who pays $2k every 6 months for their new car and that is the cheapest they could find.

If only automobile insurance was structured in a way simlar to a whole life insurance policy. Then at least you could borrow against its value. As it is auto insurance isn’t any better than insurance at the blackjack table.

Eric, your article reminded me of something my father said when I was very young when talking to another person (not me), he stated that because he hadn’t had an accident in a very long time that he was considered “overdue” for an accident by the insurance company. I grew up thinking that the insurance company was just playing with the law of averages to figure that my father was at an “increased risk” by being overdue for an accident. I no longer think this is true because when I had my first two accidents at age 16 nearly back to back, they didn’t figure my odds of having another accident would be lower since I just had 2, they said “we won’t insure you”. And those were the last 2 accidents I had. After #2 I knew I had to straighten up and drive better.

I know I’m well over a million miles now without an accident. Possibly 2 million but have no real way to go back and account for over 31 years of personal driving, delivering pizzas through college, and the over 60,000+ miles I have driven every year for work since college for an accurate number.

With that in mind, I had been with Progressive for years with liability only insurance. When I got my newish truck and needed full coverage, they didn’t say they wouldn’t insure me, but they wanted a huge premium. Which did seem insulting considering all the years I had paid and paid without making “them” pay. I did what I had to do with Progressive to get the truck off the stealership’s lot but went to an insurance broker who got me a premium that was much more reasonable. And I guess the Progressive “computer” figured out I was one of those cash cows who wasn’t paying “them” anymore and when it came time to renew insurance on my truck, they were more than happy to lower my rate vs. who I was paying at the time. I didn’t go shopping for insurance either, my insurance broker called me and said they could lower my insurance rate. When I found out from my broker that it was Progressive, I wanted to tell them to pound sand but money talks, especially when its money coming out of my pocket at gunpoint (required by gov’t).

As I had heard someone say, ‘I’m happy to pay my fair share of taxes. I would be even happier paying my fair share if it were 50% less than today’s rate’.

I’m kind of shocked the insurance twat didn’t respond, “Because of Covid”. That seems to be the answer I get to everything these days.

30 years of buying car insurance at 225 USD per month average, you’ll have a total expenditure of 2700 dollars for twelve months times 30 equals 81,000 dollars. A small fortune for the poor.

You’d be able to go to a Barrett-Jackson auction and buy a collectible Ford or Chevy.

Home insurance at 1000 dollars per year is going to be 30 thousand dollars.

Health insurance at 1200 per month will be 14,400 dollars in a year. After 30 years, you spend a sum of 432,000 dollars.

At the end of it all, you will pay the amount of 543,000 dollars for all insurances.

Property tax will probably total after 30 years in the same dwelling a sum of 45,000 dollars.

You’ll spend 588,000 dollars to live in America in your own home with your own car making sure you stay alive with minimal health problems so your medical bills won’t cost you an arm and a leg.

30 years of income at 100,000 USD will be 3,000,000 dollars. You’ll have a few shekels to trade for more wampum.

Booze and hedonics are extra.

Hi Eric, I find that if I politely DEMAND to talk to the supervisor. Then maybe their supervisor, I can in most cases get the charge reversed. At the very least they negotiate. It requires an investment of 1/2-1 hour phone wait time but usually gets me what I want. Worked recently in the case of State Farm. I had to threaten to pull all our business to get the ‘Supervisor’ with any power, but I bought myself 6 more months to shop for a new company.

The insurance mafia now has arrangements with state governments to report insurance status. When switching to new companies the old company can report people as ‘uninsured’ for not paying premiums.

hit the button too fast. anyway it can lead to paperwork screw ups and problems so I understand it. Just another way to make life difficult and more expensive. No problems if the new company reports the coverage properly and no screw ups occur.

Bloodsuckers.. I went through something similar years ago with my motorcycle. The cost of theft coverage was about 1/2 the value of my bike, their attitude was I needed it in case of theft. My response was if it wasn’t stolen in a little over two years I would be ahead. It wasn’t and when I paid cash for a new bike over 20 years ago I didn’t get it and it wasn’t stolen then either and I still have the bike.