You can’t reduce the size of a 4×8 sheet of plywood to hide the rising cost of one – or shave some length off a 2x4x8 – without it being not only obvious but an issue, functionally. Try siding a house with 4×7.4 sheets of plywood, for instance.

So, instead, the price goes up. Which is really a measure of the value of your money going down.

The same has been happening for some time at supermarkets, less noticeably. Or at least in a way that makes many people not notice it because that pack of bacon they just bought still costs about the same as it cost a year ago.

Only now it’s 12 ounces instead of 16.

Fewer rolls of paper towels – but the price seem unchanged. Such illusions of economic stability are to be found in practically every aisle and on every shelf of the grocery store – the happy spell only broken when you check out your handful of stuff and discover it cost you $100 – or more – for what used to cost you $60 or less.

But the destruction of the value of money – manifested by its ominously decreasing purchasing power – is becoming impossible to not notice when it comes to products that can’t be skimmed, put less of into the same size packages.

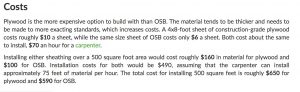

A very objective measure of how fast things are slipping – by observing how fast things are rising – is what you could call The 4×8 Plywood Index. About two years ago – in the fall of 2018 – the average national cost of a sheet of 4×8 construction-grade plywood was just $10 or so.

Fast-forward two years and that same sheet of plywood now costs $25 or more (depending on the finish). Some cost $40 per sheet. Have a look for yourself. Or do a fly-by of your local Lowes or Home Depot.

This is a 90-plus percent increase in cost – over about 24 months – a Venezuelan-style uptick – and while it it true that some of the cost uptick is probably due to temporary scarcity/increased demand – there is a building boom under way, the result of resumed construction after months of government-imposed “lockdowns” in the name of “stopping the spread” – it’s not an isolated cost uptick, which indicates it’s not just a temporary cost uptick caused by natural supply-demand fluctuations.

The cost of everything, just about, is going up. Which doesn’t reflect an increase in the value of things but rather a decrease in the value of the thing used to purchase them.

The “federal” reserve note – which isn’t even a note anymore but rather a kind of digital widget they (the central banking cartel) don’t even need to print to inflate. Just keyboard an increase in the “money supply” and – presto! – there you go.

Or rather, there you pay.

Manifoldly.

The money you are paid buys less – which means you’re working more for less – and the money you’ve saved (if you’ve managed to do so) is also worth less.

Just the thing on top of the kneecapping of millions of people’s small businesses by the government which is the frontman for the banking cartel – not “the virus,” which didn’t “lock down” anyone.

Much less “inflate” anything.

America is becoming Venezuela, courtesy of the government and the central banking cartel – but many Americans (probably like many Venezuelans) do not see it happening even as they pay for it as it’s happening. Like seagulls pecking at a piece of tinfoil at the beach, they do see the $1,400 (plus the previous $600) “stimulus” checks they got from the same government that is responsible for causing things to cost a great deal more than what they got.

This is both an epic con as well as epic testimony to the innumeracy of many Americans, especially those who supported the president selected.

Some of them may be unworried about the 90-plus percent increase in the cost of a 4×8 sheet of plywood and the doubling in cost, just about, of a 2x4x8 – which does not affect them directly if they already have a house, for instance – or are not looking to remodel it.

But do they notice they’re paying $6 for a 12 oz. package of bacon that used to cost the same or less for a 16 oz. package? It is possible they don’t as things look more or less the same – provided you don’t look too closely. Provided you don’t think too much about the fact that a pack of bacon is no longer enough for the family’s breakfasting needs. That two packs are now needed to feed the same bunch the same amount.

The one thing they cannot help but notice is the increased cost of a gallon of fuel, now about $2.88 (and rising, inexorably) according to the American Automobile Association (AAA). That amounts to an increase of about 30 percent in the course of about three months.

I wrote a few weeks back about the fact that this rising cost all by itself vitiates the value – the buying power conferred – of the “stimulus” checks, plural. Americans are paying at least an extra $12 or so to fill up the average-sized car’s tank – which works out to about $40 more per month they no longer have to buy things with, including 4×8 sheets and 2x4s and bacon.

In a year’s time – assuming the cost of gas doesn’t increase even more – or rather, that the value of money doesn’t decrease even more – this one line item will have reduced their buying power by at least $480, not counting the increased cost of things like 4×8 sheets and 2x4s and packs of downsized bacon.

If nothing changes over the next four years, what has already changed will cost them at least $1,920 – almost exactly what they received in “stimulus” from the government fronting the banking cartel.

Stalin’s chicken is clucking, somewhere.

Some of the rising cost of fuel is, of course, due to the fact of the president selected’s “executive actions,” including the cancellation of the Keystone pipeline and a “pause” in the issuance of new leases to extract oil and natural gas on land owned by the federal government. But there is – once again – the ominous fact that prices are rising generally.

Which indicates the value of money is declining, accordingly.

Which is something people ought to be worrying about a lot more than “the virus,” which has only cost them their freedom and peace of mind.

This could cost them whatever they have left.

. . .

Got a question about cars, Libertarian politics – or anything else? Click on the “ask Eric” link and send ’em in!

If you like what you’ve found here please consider supporting EPautos.

We depend on you to keep the wheels turning!

Our donate button is here.

If you prefer not to use PayPal, our mailing address is:

EPautos

721 Hummingbird Lane SE

Copper Hill, VA 24079

PS: Get an EPautos magnet or sticker or coaster in return for a $20 or more one-time donation or a $10 or more monthly recurring donation. (Please be sure to tell us you want a magnet or sticker or coaster – and also, provide an address, so we know where to mail the thing!)

My eBook about car buying (new and used) is also available for your favorite price – free! Click here. If that fails, email me at [email protected] and I will send you a copy directly!

{kind=link}

The current situation is even more dire than most people realize. The reason is that the US dollar is the world’s reserve currency. That has allowed us to live beyond our means and to export much of the inflation for decades. If we lose the reserve currency status, the living standards of most Americans will fall so dramatically that the country will be unrecognizable. One can imagine caravans of Americans heading across the border in search for a better life.

America has been binging on cheap Chinese goods for decades. And China has acted like we are going to pay for those goods eventually. If they realize that we intend on paying our bar tab with money that we printed out of our basement – or to just walk out without paying at all, they will come for our assets.

There will only be very very expensive American goods for sale when there are any goods at all. (There won’t be any electronics or computers or appliances until we figure out how to make those things ourselves.)

Printing trillions upon trillions of US dollars is almost surely alerting the world to the fact that we have no intention of paying for any of the goods that they have sent us – at least not with anything of real value. It is just a matter of time before the reality comes crashing down. To be fair, this reality wasn’t created by Biden. It has been building for decades. But Biden’s spending is going to speed up the inevitable.

I’m amazed that the science-based economists are just fine with an infinitely variable definition of a dollar. The NIST is always getting a better definition of a second, the International Bureau of Weights and Measures is always refining the length of a meter (and trying to find a way for anyone to accurately measure it), but economists are happy to have everything be relative. Then they wonder why nothing they predict ever works out.

https://www.nist.gov/blogs/taking-measure/everyday-time-and-atomic-time-part-one

Speaking of ammo, it’s been 10 years or so the federal govt. ordered huge quantities of ammo. They bought huge amounts of M 16’s and Beretta 9 mm’s. They ordered billions of rounds as did every damned federal agency including BLM, Parks and Wildlife, etc. etc. and ordered even more ammo.

I believe that the government is continuing to buy the ammo that the criminal class in charge of the gun and ammo companies are happy to oblige. It is easy to hide any expenditure now that the government is spending $3 trillion at a time. Think about it. There has been an increase in fire arms purchases at the retail level. And Ammo, but not in proportion to the shortages we are seeing. Someone is buying far more in excess than what the public at large is buying. It is the government.

Hi Swamp,

I think it’ll be interesting to see whether most people just baaaaaaaaa! and hand over their weapons and ammo when both are banned – or more likely, when it is required that in order to keep them you must pay the government $800 annually, register them and perhaps be psychologically evaluated… during which any questioning of Sickness Psychosis will result in your being labeled “unstable.”

Inflation is part and parcel with practically every action in play by government, at the behest of its bank cartel masters. Extract what wealth remains among the 99.9% and deliver it to the 0.1%. A pity it’s working so well. Guess who gets first crack at the newly created out of thin air money. If you guessed the bank cartel and its cohorts, go to the head of the class. They get it before prices are affected, buy assets they KNOW are going to increase in price, and pocket the difference. Just like they buy commercial property now distressed by the COVID “final solution” for pennies on the dollar. The intent is to make the 99.9% completely dependent upon the largess of the state. In other words, slaves.

Given the current environment where people are unable to tell time, make change, or actually sign their name, is it logical to assume they would understand inflation?

A very simple concept has been sent to realms of economists. Why I don’t know.

I would argue that most children understand the concept of inflating a balloon. I would further argue that those same children as adults don’t have a clue what inflating the money supply actually is.

The same concept applies to both. Why do people people think that adding air to a balloon is totally different than adding money?

How is it that when people grow up they become totally bereft of very simple concepts?

Not long after silver was removed from US coinage, my mom sent me to the store with a dollar bill to get a dozen cans of Campbell’s soup. She was expecting me to use the change at the soda fountain next to the IGA.

Mom was surprised to see me home in record time. I only had 11 cans and a penny. Soup went up 50%, from 6 cents to 9 cents a can.

As the Soup Nazi would say, “No ice cream soda for you!”

Since I have inflated balloons, air mattresses, and rafts, I know that it takes a concerted effort to get the job done. It’s a got-damned chore!

Why is it the products the Local Friendly Government Youth Propaganda Camps think inflation is a natural occurrence?

As they say, that thing ain’t gonna blow itself.

Good morning, T!

I think, to answer your question regarding inflation, it has to do with not respecting money as much as it does not understanding it. When manna rains from the skies – or at least, from Washington – and almost anyone one can debt-financed almost anything – why bother about the cost of things?

Or who pays?

Eric,

“ to answer your question regarding inflation, it has to do with not respecting money as much as it does not understanding it”

Hell Eric! That is the answer to so many things these days.

How can someone with no self respect or respect for others even care.

Adam Carolla wrote In Fifty Years We’ll All Be Chicks. He was a bit optimistic. This country has morphed into the land of dumb blondes.

https://youtu.be/S9Wi3A3skb0

Over two generations of Americans indoctrinated and not educated are now bearing rotten fruit. Basic economics and civics have all but vanished from the public schools and higher “learning”. The powers that be are either stupid or have ill intent. I’m betting on the latter. They know to destroy the currency is to destroy the Constitutional Republic and to usher in their oligarchy/dictatorship they’ve been plotting and scheming on since Great Society of the 1960’s. And to speed up the process, they throw the borders wide open to hundreds of millions 3rd worlders to overwhelm and collapse the economy. Dark times are indeed a coming.

On dimensioned lumber, they have been cheating those for a long time.

2X4 kiln dried sanded dimensions.

1971 1.875″ x 3.875″ (the old shop out back)

Ones I bought last year, 1.625″ x 3.375″

Explains why they keep updating the building codes. The codes have to reflect the shrinking, weaker lumber.

I just bought a sheet of ply in Australia. $45 for 1200 X 2400 mm X 9 mm thick, came all the way from Chile. A few years ago it was made in Australia, but the shutting down of the lumber industry is wreaking havoc with prices and availability here of timber products. Courtesy of the green movements.

Tudopeistan (formerly Canada)

Cheap gas, $5.25 (us gallon)

Basic 8′ “2×4″ is now $8.20 here.

Basic 1/2” 4×8 sheathing is $61

This is in the middle of a province where we pump, grow, cut and fabricate the stuff. Insane.

It is true you cannot easliy change the size of modular building products, but bulk materials can still be fiddled with.

The standard size of a sack of cement is 94 lb, because this is (approximately) the weight of one cubic foot of powdered cement. I didn’t think anyone would attempt to F* with this, but here it is:

https://www.alpinematerials.com/product/txi-type-iii-cement/

$16 for a short weight sack weighing 91.5 lb, from TXI, which is a major manufacturer.

Walmart is advertising 47 lb (1/2 sack) for 13.37, which would be $26.74/sack if they had any.

Lowes normally stocks TXI Riverside Cement. At present, their website shows a graphic of a competing mfgr., but states they have none available. The price listed is $12.48 per 94 lb sack.

I paid $10.30/94 lb last August @ Larry’s in Corona, which is slightly more than Lowes was charging for TXI at that time.

I predict that gasoline will commence being sold in liters in the U.S. before too long.

The “official reason” will be to “conform to international standards,” which is actually legit.

The entire rest of the world uses metric system – U.S. is only oddball country.

Conveniently enough, though, one liter is very close to one U.S. quart (we already have liter soda bottles in the U.S.). Posting the price per liter will “seem” so much cheaper, except that nobody will be fooled.

The late Bill Hicks had it right…

TB, the UK still use a mix of the measuring systems.

Did not know that.

Do they still have Whitworth fasteners? LOL.

Actually, U.S. also uses both systems to some degree.

My 1985 Ford Ranger had metric engine, but SAE everything else.

Ford, of course, had a close relationship with Mazda, which may have made a difference, back when.

I have been involved with U.S. construction projects for which the design drawings were all “soft metric,” which means the actual components (CMUs, doors, etc.) were sized in U.S. customary units (a.k.a. “Imperial”) but the plan dims were in mm.

These were all U.S. Government projects.

Eric,

“ Such illusions of economic stability are to be found in practically every aisle and on every shelf of the grocery store ”

The thing no one wants to talk about.

The 16oz can now has a concave bottom so it only holds 14.5oz. The 12oz beer bottles and cans now hold 11.2oz.

But my favorite is the “new” half gallon. 52oz.

When will a South Park style European Fecal Standards and Measurements Board be instituted in this country?

All those cars with a 16 gallon tank will hold almost 20 gallons. Sure the MPG will go down, but that will be a feature not a bug. All the more reason to go electric.

Will the people educated in the government schools, who can not write in cursive, or tell time on an analog clock, be able to tell the difference?

After all, hundreds of millions in this country wear a mask that comes in a package claiming they are “ineffective at protecting against the spread of COVID-19.”

This is very old story. I call it the “incredible shrinking candy bar trick.” Many years ago you could buy a candy bar from a vending machine for, IIRC, US$0.05 (a “buffalo” nickel, back when dimes, quarters, and larger coins, which did exist, contained actual silver).

When inflation happened, the price of the candy bar did not change, but the weight decreased.

“Marketing” scumbags could truthfully(?) tout “still only a nickel.”

Oh Henry bars have been my marker.

1985 ~$0.25 for 85 or 105 gram bar.

2021 ~$1.75 for 42 gram bar.

And bacon. Just saw a 220gram package for $7.99. 15 years ago, same store, same bacon, 454 gram for ~$4.00

Keep your eye on the *width* of rolls of toilet paper.

Easy to gauge this by the gap between the end of the roll and the end of the t.p. holder rod. Also easy to conceal any shrinkage in width by making it very gradual.

If you are the inquisitive sort, you might pull a tape on a roll whenever you stock up, and keep a log (of the measured widths, that is).

Had not considered width.

All kinds of tricks out there. Found an old TP 24 pack bag a while back. They have reduced the length of each ticket, but same number of segments. Roll is several feet shorter than two years ago.

I recently picked up several different packages that were on sale and the differences are amazing.

The Cottonelle “double rolls” actually seem a good deal as the are tightly wrapped large rolls. They last for a very long time.

The Purex ones are the worst. Hold one up to the light end on and you can see light between the layers as they are so loosely wrapped. Need replacing every couple of days.

Both the same package price and number of rolls, but about 5x the product from Cottonelle.

But no worries, TVs and phone screens are getting bigger!

>Hold one up to the light end on and you can see light between the layers

Sounds like a real “breakthrough” in t.p. technology.

>millions in this country wear a mask that comes in a package claiming they are “ineffective at protecting against the spread of COVID-19.”

Which some of them ignorantly refer to as PPE.

Protection against what, exactly?

Turtle,

“ Which some of them ignorantly refer to as PPE.

Protection against what, exactly?”

Pardon my French, but they are protected against the fucking bogeyman. Or as I like to call it, la chupacabron.

Maybe we should call it what it really is – CHUPACOVID.

Todos de ellos son pendejos, por cierto.

Que comen mi verga, todos los políticos.

I call it conjob19.

The building boom is coming to a halt very soon. Just as it did in 2008, but only worse. So called starter homes can’t increase from $170,000 4-5 years ago to $350,000 as it has done in my area. I don’t care about all the people “moving from California” that everyone shrieks about. It’s just a matter of time until those people are unable to sell their homes at ridiculous values and buy “cheap in Idaho, Utah and Montana. It’s just not sustainable. It hasn’t set in yet, but there are already people stopping plans of building because of the cost. There is a shortage of building lots right now but it will quickly change to a surplus as people stop building. Then there will be empty lots with panic among developers who will try to unload them. It will take years for their “value” to come back up, if Uncle can get himself out of this jam.

I didn’t think they’d pull off a way out of the jam they created in the late 2000’s. But they did. It’s orders of magnitude bigger than last time. I see no way out of having a major meltdown. I also see no way of coming out of it with any semblance of civilization as we know it. But I’ve been wrong before. I believed there would be worse than the great depression circumstances last time. Now , here we are and I don’t know what to think other than when it does end, it will end very badly.

Stagflation is a real possibility. The weirdest thing is that the lumber yard I drive past every so often is stacked to the gills with lumber like I’ve never seen before. So supply seems to be way up but prices have continued to go up. Construction continues, though mostly on speculative stuff and by folks who, like a number I have actually heard this from, are doing reno work, roofs, etc. now, to get ahead of expected inflation.

‘The building boom is coming to a halt very soon. Just as it did in 2008 …’ — ancap

Overheard a couple of women in Walmart this morning, talking about zero-down USDA property loans. Funny, USDA loans were brought up last week by another couple I know, who also mentioned they are on the verge of eviction.

When folks who don’t even have ‘ninety-nine dollars and a dream’ (as ol’ groper Bill Clinton used to say) are itching to punt on nothing-down real estate, you can be pretty sure they’re gonna get not merely their fingers, but their WHOLE ARM burnt off, just like last time and the time before that.

As Carlos Santana might have said, ‘Those who do not learn history are doomed to repeat it.’ 🙂 🙂

**”As Carlos Santana might have said, ‘Those who do not learn history are doomed to repeat it.”**

LOL!!!!! Good’un!

Jim,

“ As Carlos Santana might have said, ‘Those who do not learn history are doomed to repeat it.’ ”

Exceptionally smooth comment Mr. H.

https://youtu.be/6Whgn_iE5uc

T. that made me feel so much better. Love that song and I thank you.

Yep.

Same thing happened in the stock market in the 1920s. When the shoe shine boy is touting stocks, you know the crash can’t be far off..

Here in western Riverside County, CA 92882, housing prices are headed for “nosebleed” territory, just as they were a dozen years ago. The fallout from that bubble was >50% decline in housing prices, from ~500,000 to ~225,000 for adequate single story frame-stucco boxes built after WWII.

From what I can see, we may be on the cusp of another bust here in Corona.

Two data points from Zillow:

1100 s.f. built in 1947 sold in 11 days for full asking price of $460,000

1132 s.f. built in 1947 sold 10/20/20 for $455,000

Present Zillow estimate of latter sale is $490,000

If accurate, price inflation of 35/455 = 0.0769 in 5 months

=> (0.0769)(12/5) = (0.0769(2.4) = 0.28 per 12 months

These houses are nothing special, and not built to modern electrical service or insulation code. Single story post WWII stucco boxes (similar to my own, which built in 1956).

FWIW, similar property in Orange County, or Pasadena, would fetch at least double.

This cannot last, IMO.

Hi ancap,

If people stop building how does this cause a surplus? To me this would cause an even larger increase in the value of existing homes. A lot is worthless unless some type of dwelling can be structured upon it. The builders can try selling the lots for cheap, but if the materials to build it are not available nor the tradesmen, it would be a foolish purchase. This would mean current homes would skyrocket even more. As of now there is a shortage in available homes, hence the increase in price. I see very little similarities between this pending crisis and that of 2008.

Do I believe home prices will eventually moderate? Yes, but I don’t see this happening in the near term.

Hi, RG,

I believe ancap was talking about building lots, not finished houses.

In many cases, land developers subdivide raw land, and either sell the permitted tract, or the actual finished lots, with utilities, to a “merchant builder,” who builds the actual structures. Of course, the larger builders can do the entire process, from raw land to houses for sale.

The land development process is expensive and time consuming, at least here in SoCal. Five years from raw land to approved tract map is common. There are many “hoops” which must be jumped through, and a developer of my acquaintance tells me many more hoops may be added during the development process, as the laws change.

The question is, at what stage does the “music” stop, and who gets stuck with the loss? Economics favors the large operators, who can better(?) afford to sit on land they have developed themselves until market conditions improve.

If the music stops during actual “onsite” construction, you get ghost towns, as were common during the Reagan recession of 1982. First the builder goes bankrupt, the construction lender forecloses and takes a loss, and the property sits abandoned until the lender can dispose of the REO, which will not happen until it makes economic sense for another builder to buy the unfinished project.

in the early 1980s, it was the price of money (mortgage loans) which killed the housing boom, which had in turn been fueled by high inflation of late 1970s. At the time, I was earning my living as a framing carpenter in Orange County, California, and had a front row seat. There was a long “overshoot” before the market collapsed. I bought my house (still live here) in 1981, which was a great year for me, and willingly paid 16% (+ 1/4 PMI) for mortgage money, because I desperately needed the tax write off. Many others were in the same circumstance, because marginal Federal income tax rates had not been re-indexed to reflect price inflation of the late 1970s. The average working stiff could, and did, find him(her) self in the 70% marginal tax bracket. The only way out was to seek (tax) shelter via mortgage interest tax deduction. “Gimme shelter,” indeed.

Hi RG,

I was speaking of subdivision lots having a surplus.

In my area in Idaho, existing home sales have dwindled very low over the past 6 months. Houses are selling for a premium, but buyers are almost always from out of state–usually California–because people from here cannot afford to build or buy a home. Three years ago you could buy a new 2400 square foot home in a subdivision for $170,000. Today, you cannot touch that home for under $350,000. Last August you would have paid $240,000-$270,000. Now subdivisions are going in as fast as they can do them. Many people have already delayed building a home because of the high costs. What happens when many more wait? You end up with millions of dollars worth of infrastructure in and on the ground with no one willing to buy because the house is too expensive to build. That’s when things get out of control.

I am in the excavation industry. I was in it in 2008. I’d like to say I’ve seen this before, but 2021 is 2008 on stilts and anabolic steroids. 2008 was just a microscopic shadow of what I’m seeing today. What I’ve seen is nothing compared to how bad this will end. The longer it takes to implode, the worse it will be. That’s the only thing I know for certain.

I paid $170,000 for my 2900 square foot home on 1 1/4 acres in December of 2008. In June of that year It appraised for $195,000 but no one could buy it in 08 because of the bust and difficulty getting loans at the time. I could list my house for $450,000 right now. I’d get a bidding war between 3-4 Californians and it would sell for $500,000. But I–and hundreds of others– don’t do it because it would cost that or more to replace it right now. It’s only people that haven’t lived and work here that can afford to do anything.

This type of insanity in the market is completely unsustainable. I’m astounded buy anyone that believes it is.

Hello Ancap. I bought a house and land separately in rural Australia in 2000. 1 acre near the end of a court, near by access to freeway and rural train services to Melbourne. $250k for h&l. 2 years later put up a 7X9 meter barn. Our area is exclusively acre and above lands. house is modest, 22 squares, 2 car garage all brick on elevated slab. 2 houses on our street sold recently each over $800k. Our suburb, once rural, is now all built up, dense traffic even in offpeak hours. Our land and houses are still much cheaper than anywhere else near Melbourne.

Our house is almost paid off. Except now you don’t get a title after paying off the mortgage. Apparently all Australian land titles are held in the US by a company called Perpetual Trustee. Of course our banks don’t tell you this. So theoretically you can pay off your house and still not own it.

How is the US dealing with title to the house on paying it all off?

Hi to5,

I paid off mine in December and the mortgage company sent us the deed stamped “Satisfied.” Basically the deed is nothing more than a copy of the court house’s record with your name, address, map ID, etc. on it, but it is something.

Hello, to5,

In the U.S., you get what is known as a “full reconveyance” upon paying off the loan. The legal term for putting up the property as security for a debt is called hypothecation. You can look up the Wikipedia article for details. The owner retains legal title, with the power to rent or sell the property, but the title is said to be “encumbered” by the debt. Paying off the debt removes the encumbrance. That is when you are entitled to a reconveyance. In California, the usual legal instrument used to encumber the property is a Deed of Trust:

https://www.lawdepot.com/law-library/faq/deed-of-trust-faq-united-states/#.YGjsuHvPwzM

I don’t know about Australia, but I read that in Canada, title to all real property remains vested in the British crown. Perhaps someone can explain this (or debunk, if incorrect).

You dig deep enough in Canada, EVERYTHING belongs to the crown, you included.

Even the Charter of Rights and Freedoms here, supposed document to protect the individual, is treated as a mere suggestion of no binding by the courts.

Land Titles are handled by each province. Property transfer (such as it is) is just the lawyer sending a document to the Land Titles Office stating the PID transfer and parties. You get a document showing the transfer to the new, I shit you not, tenant. That is the legal description of the “owner”.

https://www.bclaws.gov.bc.ca/civix/document/id/loo69/loo69/02_53_90_02a

At least they’re honest about it. Here in the U.S. you’re told when you buy real estate that it’s “your” property – as long as you keep paying rent (property tax) to the armed thugs of course. (“Your” property is also used as collateral when your municipality goes into debt.)

Hi Jason!

I regard the tax on property as far more an affront – and dangerous to liberty – than the tax on income. If it is possible to truly own your land/home then you can avoid the tax on income because little “income” that is taxable is required to maintain oneself on one’s own land. Most people could live comfortably on $1,000 a month or less – at the “poverty” level, as far as the tax code defines it. But rich almost beyond dreams in being beholden to no one and living well – and free.

Here in Missouri, and I assume likewise else where, the other aspect of property taxes that is equally abhorrent, is that most of it is applied to the by far most successful, and evil, psychological operation in history. Public “education”. My tax bill is broken down by what “services” it pays for. Public “education” gets about 3/4 of it.

Ditto in Idaho John.

3/4’s of my taxes are “for our children”. Never mind it’s for “their” children because I homeschool.

If they don’t get their local skuuul bonds passed, they vote six months later. They do it until it passes Eventually everyone gets sick of going to vote no so they round up enough votes to pass them.

Morning, Eric,

All taxes ae evil, of course, with only a few of them (arguably) a “necessary” evil.

For me, the (intentionally?) misnamed “income tax” may be the most evil.

Why? Because it is really a tax on productivity, not on income.

The average wage earner does not realize this, because “income taxes” are over-withheld from his paycheck, and he is conditioned to be thrilled to get an annual “refund” of money which was stolen from him at zero interest for a year. Clever, hey?

Those of us who are self-employed know that, in order to pay our “income tax,” we must earn additional income, which is itself taxed. The more you earn, the more you must pay. Earning at a higher rate requires paying at a higher rate.

Sort of like a tractor pull.

A cynical person might deduce that the intent is to keep the citizen (a.k.a. “taxpayer”) in perpetual debt bondage to “his” government.

I, of course, would never be that cynical.

Would you like to buy a bridge?

> How is the US dealing with title to the house on paying it all off?

I bought a condo in Las Vegas at the tail end of 1999…moved in in January 2000. A couple of months ago, I paid it off. A week or two ago, I received the original note from the bank that I had signed 21 years ago…but with a “paid” stamp on it.

Then again, a notice of delinquency arrived last week from the county treasurer’s office because neither the bank (via escrow account) nor I had made the last payment. Total tax for the year is less than what a month’s mortgage payment used to be, but as Eric has noted on more than one occasion, do you really “own” your property if the government can yank it back?

In nominal terms, say against an ounce of gold, house prices will drop. The question becomes, does it drop in regards to federal reserve notes. This is one I’m not sure about, and has been keeping me up at night. The drooler fuher’s handlers have been been busy cranking this inflation up and I don’t know what to do. I’ve been expecting the price to drop for about 4 years. I should have bought then.

I hear you Mattacks. If I had known that land was going to fly to the highs it has, I would have bought 12 acres behind my house for the $10,000 per acre it would have taken 4 years ago to buy. I could have put in a road and power and sold two 3 acre lots for $125,000 each and kept the 6 acres directly behind my house. I’d only gain 2 neighbors which technically wouldn’t be very close to me. I’d also gain 6 acres of space and made a handsome profit through the whole ordeal, especially since I have the equipment to build the road and dig the power myself. I didn’t do it because $10,000 per acre for undeveloped property was a ridiculous proposition 4 years ago.

The millstones of inflation and taxation are grinding in overdrive. The demented diaperer will give us a healthy dose of each. Speeding us on our way to economic collapse. Yea!

Which is exactly contrary to the effect of using real money, backed by a thing that is limited in supply, doesn’t rust away, and which has value recognized world wide. That thing with limited supply being infinitely divisible, as production increases, PRICES GO DOWN! Interest on savings is unnecessary since the money you saved will simply buy MORE next year.

Several years ago, I read some of a collection of correspondence written by those who directly experienced the Weimar collapse. The tales of the amount of money one had to carry in order to live were astonishing. But the common thread that really struck me was that it did not happen slowly. It appeared abruptly, and grew exponentially. We’re in the “appeared abruptly” stage.

You know, once upon a time, there was such a thing as a three pound can of coffee. It’s been a while now.

JK,

The only problem is that, even when currency is backed by precious metal; even if one uses the metal itself (so called “honest money”); it can still be debauched; it can still be inflated away? How? The Romans showed us how to do it.

Back in Roman times, copper was a precious metal. It formed the basis of their money, which was called the As. After the Roman Empire had been around a while, they’d run in to quandary; they’d engaged in all this foreign adventurism, and were wondering how to pay for it. Sound familiar? Someone in the Roman gov’t came up with the brilliant idea to halve the copper content of the As, thus doubling the money supply! If the Romans did it, then why couldn’t the same be done with gold and silver?

At the end of the day, ALL money can be inflated away; all money can be debauched! Use of precious metals won’t automatically solve the problem, either. Rather than printing more paper, all one has to do is either reduce the metal backing the paper; or reduce the metal content of the money itself. The only thing that changes when precious metals are used is HOW they’re debauched, not if; only the method changes. Ergo, what matters most is the honor and integrity of those administering the money supply, all of which are in short supply these days…

Mark – the exception here would be that metal content is determinable (word?) and such debasement is readily apparent and even a complete dupe would understand he was being robbed (although, im not so sure of that anymore with general population).

Have you seen those Mark Dice man on the street interview videos where people choose the chocolate bar over the silver bar?

At which point it’s no longer “real money”.

I guess. My point was that any money, no matter what form it takes, can be debauched; there’s no FOOLPROOF way to stop unscrupulous people from debauching a nation’s money. The only thing “honest money” changes is the method, not the end result.

The Romans showed us how it can be done thousands of years ago. If they did it then, then it could be repeated now. As The Preacher said in Ecclesiastes, there’s NO new thing under the sun…

True – don’t forget the practice of “clipping” coins to shave off some of the precious metal…

Also don’t forget that after the Roman collapse it was a death penalty offense for debasing the coin in every Anglo western country including the US. Technically, it is still a death penalty offense in the US.

Which is the single product produced by the Federal Reserve. Counterfeit money. The profit from which is directly acquired by the bank cartel. If you dig deep in your mortgage contract, you may find as I did when I had one. The lender has the power to call that note due in its entirety anytime they please. Which means with the current level of private debt, the bank cartel now OWNS the US, and much of the rest of the world.

Funny thing you mention Weimar Germany’s inflation. I was just reading a monograph on that very topic. Even stranger, I read that the Weimar government decided to get out of the Reischmark inflation jam by pegging a new currency’s value to something of intrinsic value, but not a precious metal. They, being German, chose rye (the grain, not the hooch made from it!). It worked, but only because Germany was full of Germans, who had some degree of faith in the Roggenmark scheme, and in their fellow Germans. This sort of scheme would never work in today’s USA. A return to currency pegged to a precious metal would not either I am afraid. We’re past that point in the decay curve.

‘We’re past that point in the decay curve.’ — Crusty

Welcome to the Third World colossus of Kamalastan (formerly known as the USA), as it prepares to emulate Chairman Mao’s lethal Great Leap Forward with Joe Xiden’s Build Back Bugger debacle.

Call 1-800-DEM-PUNK to find out whether an exciting career in the Red Guards is right for you.

Jim H, laughing my ass off. Like the word dempunk.

Eric,

What concerns me is how to PREPARE for this? Buy gold or silver? Acquire a stable foreign currency? Buy tradeable items? What about fuel coupons? How does one PREPARE for especially hyperinflation?

I thought about buying gold and silver, but the gov’t will know if you buy huge quantities of it; they could later confiscate your gold and/or arrest you. FDR confiscated gold here in the 1930s. In Zimbabwe, if you were caught with large amounts of gold, they’d arrest you. Also, in Zimbabwe, gold and silver weren’t used that much as a medium of exchange; it was used more often to acquire stable foreign currency.

In the mean time, gold and silver, as investments, have problems. One, you have to have somewhere to physically store it. Two, it provides no income; there are no interest or dividends with gold and silver. They can be speculative too.

n Zimbabwe, people would get stable foreign currencies. That was illegal there, and will likely be illegal here too. Plus, all the major currencies are being inflated, so which one do you pick? I was thinking of the Chinese Yuan since they’re the next global superpower, and they’re likely to be the world’s reserve currency. The problem is that the Yuan is going digital. How does one acquire it?

Another thing that happened in Zimbabwe was people would barter toilet paper, tampons, whiskey, and so on to pay for stuff. Okay, that’s good. The only problem is that many useful items also have a useful life; they have an expiration date, so they can’t be stocked ahead of time.

Finally, one thing that became money were fuel coupons. After the Zimbabwe dollar was trashed, fuel was in short supply. Their ZD were useless, and foreign companies would no longer accept payment in ZD. So what fuel companies there did was sell coupons-again, for stable, foreign currencies-so the bearer could buy fuel with the coupons. These coupons were traded for things, and they ended up becoming a de facto money. Okay, but no one offers fuel coupons now, nor do we know who’s likely to do so.

Ideally, I’d like to prepare in such a way that I not only survive what’s coming; I can PROSPER! Someone always does well, no matter whether the economy is good or bad. Back in Weimar Germany, a chap by the name of Hugo Stinnes did very well. He was the Warren Buffet of his day.l

Eric, I don’t see any good way to prepare for the inflation that’s coming. I just read a book about Zimbabwe’s hyperinflation, and while they offer some useful info, I don’t see any good way to prepare. You’ll either be arrested if you have a lot of gold, or, if you’re lucky, the gov’t will just confiscate it. Stable foreign currencies have worked in past hyperinflations, but with all the money printing going on with all the major currencies printing, which one do you pick? I thought about tradeable items, but many of those have expiration dates; how does one stock up in advance? How does one acquire fuel coupons when they don’t, as yet, exist?

And there lies the rub. One simply cannot prepare for the actions of a government, which is composed almost entirely of sociopaths if not psychopaths. There is no evil you can imagine that is so very evil that the state won’t embrace it, if it serves its purpose. Dispose of the elderly? Already being done. Round up teenage girls, and some boys, and screen them for potential service as sexual favors for their cohorts in return for favors? Epstein.

The ONLY thing that would cure problems with the money supply is the same thing that would help solve many problems: get the gov’t the hell out of it! If people could use whatever they want for money, the market would find what works best, and that would come in to widespread use. Just like anything else the gov’t touches, money gets screwed up the moment they get involved.

Hi MM,

Looking for an investment that never expires or decreases in price…may I suggest ammo?

The increase in prices is usually associated with a shortage, what is happening now is no different. I am not disputing the devaluation of the US dollar, but demand overriding supply is more concerning to me at this point. Of course, government is still to blame since they were the ones to issue the lockdowns causing the shortages. There is a major storage coming in aluminum, steel, and lumber. New building will be halted because enough supply will not be available to complete construction. Also, think of all the items that contain these materials – soda cans, nails, computer parts, sinks, etc.

The value of an item is meaningless unless you can access the supply.

I also believe that the shortage of ammo is due not just to supply and demand, but to the government’s interference in availability of components, as well as its pulling the strings to prevent manufacture and/or gobble up supply so that ammo is effectively unavailable to the average person.

Without a doubt. That is what makes it valuable. 😊

Without a doubt there’s something else going on with ammo. Yes, there is probably a greater than usual demand, but the fact is that, at least in my area, supply is ZERO, and has been for about a year. I could see it if the shelves got stocked and then sold out real quick, but my regular dealer, (and others that I have visited) hasn’t been able to source anything since last spring. I smell a rat.

Me,too. A year with NO availability. Like everything else in this Alice in Wonderland scenario, nothing makes sense. The worst case is the likeliest probability.

Hi Floriduh!

A weird thing in my area – a rural area. One used to hear people target shooting regularly (legal, here;I could go in my back yard and do some target practice anytime I like). It’s been silent for months. People are conserving their ammo – or they don’t want to call attention to what they have.

Yup, I used to like to go to the range every Sunday morning. Haven’t been in over a year now. I’m afraid to shoot up my ammo, cuz it doesn’t look like I’ll be able to get any more.

RG,

Then the question becomes: what caliber(s) to get? I think I’ll start stocking up on things that don’t have expiration dates, like tampons, canned goods, whiskey, etc.

I think 9 mm is pretty standard.

You realize a single man living alone with a large assortment of tampons is going to be questionable by any chick you bring by the house, right? 😉

I would also recommend tp, canned goods, and cigarettes.

You already said canned goods. Sorry. Batteries is another one.

RG,

I’m not planning on bringing any women here; in fact, the only women who’ve been in my house are my late mother and my pet sitters. Two, I know that, in Zimbabwe, tampons were a good barter item; if a woman can’t understand the rationale behind their purchase, then do I want someone so lacking in smarts and common sense in my life? Cigarettes are good too. As for batteries, I’m stocking up on those, but it’s more for personal use. If hyperinflation hits, electricity will become sporadic; I’ll need something to power my AM/FM/shortwave radio if I can’t recharge its regular batteries. I have enough batteries to power my radio for at least a year.

RG,

“ You realize a single man living alone with a large assortment of tampons is going to be questionable by any chick you bring by the house, right? 😉”

But what if he also stocks a large assortment of dark chocolate packaged with those tampons?

I think that may border on hero status.

LOL. You are right. Add a couple bottles of wine to the cellar and she may not leave.

I keep forgetting what day and age we live in…or maybe what household I live in.

RG,

“ I keep forgetting what day and age we live in…”

You’ve already covered ammunition.

But when I’ve asked my wife what the best type of feminine protection was, she’s was always consistent. Smith & Wesson.

I’ve always had a penchant for Beretta.

I learned my ammo lesson way back in the 1990s when the “assault weapons ban” was on the Bill Clinton table, and not only did ammo disappear, but components to make it also. I’ve been building my own ammo for about 40 years. After the supply returned later in the 1990s, I stocked up. And by that I mean STOCKED UP. And continued to do so over the years. I now have not only enough components to make a lifetime supply for myself, but for at least a generation of my progeny. Mainly for two calibers, .223/5.56 and 9mm. Its good to use the same ammo the military does, so if it comes to it, you can steal it from them. Guerilla 101.

Depends on the type of collapse and how deep it goes. Very deep, probably little that can be planed for.

Hard assets like, farming equipment, fertilizers, canning supplies, and all the basic 1800s type low tech, animal/human powered equipment. But only if you are way out in the middle of nowhere. Any cache close to a city will be found and looted. Be prepared for life without gas and electricity.

All planing should start with how to hide or defend your preparations. Pointless to prepare for someone else with a gun to take.

Tampons, TP, hot bath facilities, good bedding and chocolate. Every woman will want to live in your harem. 🙂

But for serious, real, first hand experience and advice, read some of Selco Begovic and the experience in the Balkans war. Most of us can speculate, he can relate actual experience.

MarkyMark,

I’m a chemist, and such a trade should be quite useful and lucrative in times of economic turmoil.

A good investment for me have been catalysts. Many reactions are very simple, but require sometimes rare and expensive catalysts, which would likely be unavailable during these times. So, they’re good as an investment themselves, but products produced from them will also me valuable. Theoretically, they can be reused forever, but of course, there are practical limitations.

I’m doing what I can to reduce my expenses. Installing solar on the roof this summer, last year was upgrading the HVAC to high(er) efficiency since it was getting to end of life anyway, and a more efficient water heater. Reworking my phone plan to something cheaper and revisiting some of my subscriptions that aren’t used much. Actually using some of the stuff I’ve bought over the years instead of looking for more. Cooking at home, using much simpler ingredients and shopping in the produce aisle instead of buying packaged goods.

You get the idea. Little changes to habits now, and pulling expensive projects forward before the big hit comes.

‘But there is – once again – the ominous fact that prices are rising generally.’ — EP

CPI (the Consumer Price Index) is the US fedgov’s low-inflation megaphone, blaring the anodyne message ‘Nothing to see here, folks.’ In the last monthly report, inflation rose but 1.7% in 12 months.

Most folks aren’t going to pick up their pliers and screwdrivers to mess around under the hood of the CPI. But Mike ‘Mish’ Shedlock did. And what he found ain’t pretty.

Here’s the showstopper: OER (Owners’ Equivalent Rent) is the largest component of CPI, at a 24% weight. At a moment when house prices nationwide are ripping higher at an 11.2% annual rate, OER putters along at a mild 2.2% increase.

How OER is collected is even dodgier. Homeowners are asked what they *think* their house would rent for. That’s right: nearly one-fourth of the CPI is based on an *opinion* survey, not actual prices.

Using the Case-Shiller housing price index, Mish substitutes it for OER and finds that inflation is rising at 3.8%, not 1.7% (assuming the other three-fourths of CPI is accurate, despite hinky hedonic adjustments for quality which likewise depress the numbers).

https://www.thestreet.com/mishtalk/economics/hello-fed-inflation-is-rampant-and-obvious-why-cant-you-see-it

CPI is used to index everything from TIPS (inflation-linked Treasury bonds) to Social Security payments. Systematically understating CPI saves big dollars for Big Gov.

Who you gonna believe — the BLS (Bureau of Labor Statistics), or your lyin’ eyes?

https://www.bls.gov/news.release/cpi.nr0.htm

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and

can be produced only by a more rapid increase in the quantity of money than in

output.” Milton Friedman